Highlights of Dexter’s October 2024 report

Sales transactions jump in October

New listings for the month of October second highest since 1991

50-point rate cut by the Bank of Canada – more to come!

Listing absorption rates spike

After a September of promises, seems the only one that was delivered was that of more sales in the real estate market. This on the heels of a jumbo interest rate cut by the Bank of Canada. Although jumbo is a subjective term. A 50-basis point reduction could probably be called minimal, with a 75-point cut more warranted given current economic conditions. With the Canadian economy flat, inflation well below target and jobs numbers less than ideal, it’s more like the Bank of Canada bunted instead of swinging their bat! And now with the provincial election in British Columbia seemingly settled, will it be four more years of an NDP government promising more housing on policy that that continues to bunt instead of swinging for the fence? Or will we be back to another election sooner rather than later? Perhaps October was a sign that some buyers are tired of waiting and decided to jump back into the market despite all this political noise.

We continue to see a distraction coming from the United States with their Presidential Election today and their Federal Bank’s rate decision in the days after. The U.S. has some catching up to do with Canada in terms of interest rate cuts and as a result we’ve seen the Canadian Dollar drop to lows last seen in 2020. With the U.S. Economy performing better than Canada, it’s unclear how much the U.S. will cut their rater in 2024. This could mean a lower Canadian Dollar as rates continue to come down in Canada with the Bank of Canada potentially dropping by another half percent in December and again in January. Economic headwinds may continue to be a distraction.

There were 2,632 properties sold in Greater Vancouver in October, after 1,852 sold in September, 1,903 sold in August, 2,333 properties sold in July, and 2,418 sold in June. This was the highest number of sales since May. Will October be the peak of the fall market? Based on seeing a greater percentage of sales occurring in the first half of October, November will likely see less activity. But that is typically the case. Given the half percent interest rate drop by the Bank of Canada in late October, anything is possible though. The only time in the last 30 years we’ve seen November outperform October has been in periods coming out of a slow market cycle. Anecdotally, there was a tone of greater buyer engagement after the October 23rd rate announcement, some properties that had been sitting were getting activity and even offers, and with another Bank of Canada meeting on December 11th, this trend of buyers engaging is likely to continue, especially with another “jumbo” rate drop in December likely.

Sales in October were a 32% increase from the 1,996 properties sold last year and a 37% increase from sales in October 2022. This after 5 successive months of year-over-year declines for sales totals in Greater Vancouver. This month-over-month increase in sales is the highest we have seen for the month of October going back 30 years and the highest increase for a month since early 2022 coming out of 2021. Something was different this October for buyers and that could be the signal that sales activity is swinging back after a period of below average sales. With new mortgage rules coming into effect in December that will allow buyers of presales to increase their amortization period to 30 years and an increase of the threshold for insured mortgages to $1.5M for first time buyers, this could add more demand into the new year. We’ve said it before and this could be true projecting into 2025, buy now or compete later.

Sales in October were 5% below the 10-year average, a significant improvement over the last few months where September was 26% below the 10-year average, August sales 26% below the 10-year average, July at 18% below the 10-year average and June at 24% below the 10-year average. This was not just a seasonal adjustment. October sales showed a recognizable improvement in market activity. While April and May sales in 2024 were slightly higher, October’s promise seems to be a better sign of the market to come.

In Greater Vancouver the number of new listings in October declined from September but were the highest for the month of October since 2020 and the second highest for the month of October going back to 1991. Sellers are still participating in the market although some of those listings may be properties taken off and relisted at a lower price as sellers adjust to market activity and buyer patience. With 5,577 new listings in October, this was a 10% decline from the number of new listings in September and a 17% increase from the number of new listings that came out in October 2023. Listings will help provide opportunities for buyers who will engage in the market through the remainder of 2024 and those savvy buyers will look to take advantage of any opportunities that exist.

The number of new listings in October were 20% above the 10-year average after September was 16% above, August 1.5% below, July 12% above, and June 2% above the 10-year average. With 2 months left in the year, the total new listings for the year are already ahead of 2023 and will finish with more than 60,000 in Greater Vancouver. This will likely be the second highest annual amount in the last 10 years on the heels of 63,711 in 2021. While on the high side, it is still not high as 1992 to 1996 where the number of new listings in those years averaged 63,452. But as a percentage of total housing stock, there are far few homeowners listing their properties for sale compared to 30 years ago. And with the 2-year ant-flipping tax of 20% being introduced by the B.C. NDP in January 2025 (retroactive to the previous two years), this will lead to less homes being listed. And if you are hoping to buy a home someone has renovated so you don’t have to, there will be less opportunity for that starting in January.

There were 14,477 active listings in Greater Vancouver at month end, compared to 14,932 at the end of September. After being up 46% year-over-year at the end of May, currently there are 25% more active listings year-over-year, a drop from being at 31% at the end of September. And with several listings expiring on October 31, the total number of active listings at the start of November dropped to 14,104. Even with the higher levels of new listings, Greater Vancouver still didn’t hit 15,000 total actives and hasn’t seen that number since 2019. Looking back, between 1995 and 2000 total active listings were above 15,000 for that period. This was like the stretch of 2010 through 2014 where most months saw over 15,000 active listings in Greater Vancouver. As the year finishes, total active listings will continue to decrease and may finish below 10,000.

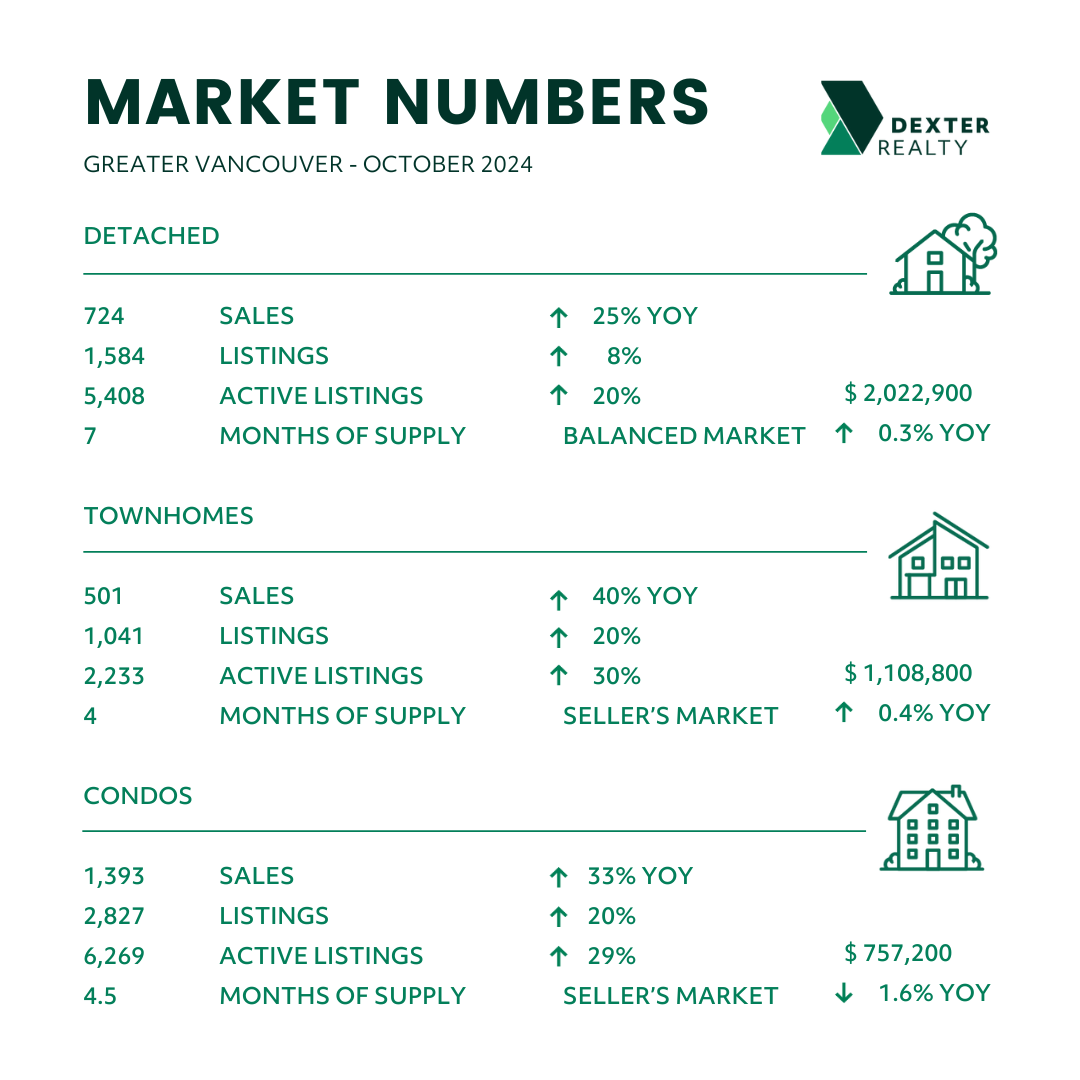

Months of supply dropped in Greater Vancouver in all markets and segments. Overall, the detached market in Greater Vancouver is down to 7 months supply from 11 while townhomes dropped to 4 months from 6 (technically a seller’s market) condos dropped to 4.5 months from 7. Not surprising that as mortgage rates decline, activity in the multifamily segment increases. Increased sales in all areas and types of homes in October brought inventories down and with the higher sales created more competition amongst buyers for new listings as well as those active on the market. Townhomes and condos are sitting at 30% and 29% above last years’ active listing counts while detached homes are only 20% above the levels at this time in 2023.

October showed a significant improvement in sales activity, which is above what is seasonally typical. Driven by the townhome market, the missing middle continues to be the most difficult to get into for buyers. One month doesn’t make a trend but with continued interest rate reductions, it’s highly probable that activity in real estate will continue to improve. How much so is very much dependent on economic headwinds that are ahead, not to mention political distractions that will continue.

Here’s a summary of the numbers:

Greater Vancouver: Total Units Sold in October were 2,632 – up from 1,852 (42%) in September, up from 1,903 (38%) in August, up from 1,996 (32%) in October 2023, up from 1,923 (37%) in October 2022, down from 3,545 (26%) in October 2021, down from 3,787 (30%) in October 2020, and down from 2,892 (9%) in October 2019; Active Listings were at 14,477 at month end compared to 11,599 at that time last year (up 25%) and 14,932 at the end of September (down 3%); the 5,577 New Listings in October were down 10% compared to September 2024, up 17% compared to October 2023, up 36% compared to October 2022, up 35% compared to October 2021, down 2% compared to October 2020, and up 33% compared to October 2019. Month’s supply of total residential listings is down to 6 month’s supply from 8 (balanced market conditions) and sales to listings ratio of 47% compared to 30% in September 2024, 42% in October 2023, and 47% in October 2022.

Month-over-month, the house price index is down 0.6% and in the last 6 months down 2.8%.

Vancouver Westside: Total Units Sold in October were 472 – up from 312 (51%) in September, up from 337 (40%) in August, up from 352 (34%) in October 2023, up from 342 (38%) in October 2022, down from 595 (21%) in October 2021, down from 547 (14%) in October 2020, and down from 506 (7%) in October 2019; Active Listings were at 3,106 at month end compared to 2,629 at that time last year (up 18%) and 3,174 at the end of September (down 2%); the 1,138 New Listings in October were down 13% compared to September 2024, up 14% compared to October 2023, up 32% compared to October 2022, up 17% compared to October 2021, down 3% compared to October 2020, and up 39% compared to October 2019. Month’s supply of total residential listings is down to 7 month’s supply from 10 (balanced market conditions) and sales to listings ratio of 41% compared to 24% in September 2024, 35% in October 2023, and 40% in October 2022.

Month-over-month, the house price index is down 1.5% and in the last 6 months down 3.5%.

Vancouver East Side: Total Units Sold in October were 282 – up from 211 (34%) in September, up from 193 (46%) in August, up from 231 (22%) in October 2023, up from 194 (45%) in October 2022, down from 394 (28%) in October 2021, down from 392 (28%) in October 2020, and down from 316 (11%) in October 2019; Active Listings were at 1,512 at month end compared to 1,265 at that time last year (up 20%) and 1,529 at the end of September (down 1%); the 613 New Listings in October were down 21% compared to September 2024, up 8% compared to October 2023, up 40% compared to October 2022, up 28% compared to October 2021, down 11% compared to October 2020, and up 6% compared to October 2019. Month’s supply of total residential listings is down to 5 month’s supply from 7 (balanced market conditions) and sales to listings ratio of 46% compared to 27% in September 2024, 41% in October 2023, and 44% in October 2022.

Month-over-month, the house price index is up 0.8% and in the last 6 months down 0.6%.

North Vancouver: Total Units Sold in October were 224 – up from 144 (55%) in September, up from 145 (54%) in August, up from 194 (15%) in October 2023, up from 195 (15%) in October 2022, down from 263 (15%) in October 2021, down from 334 (33%) in October 2020, and down from 260 (14%) in October 2019; Active Listings were at 848 at month end compared to 627 at that time last year (up 35%) and 856 at the end of September (down 1%); the 492 New Listings in October were down 9% compared to September 2024, up 32% compared to October 2023, up 42% compared to October 2022, up 66% compared to October 2021, up 9% compared to October 2020, and up 43% compared to October 2019. Month’s supply of total residential listings is down to 4 month’s supply from 6 (seller’s market conditions) and sales to listings ratio of 46% compared to 27% in September 2024, 52% in October 2023, and 56% in October 2022.

Month-over-month, the house price index is down 1.0% and in the last 6 months down 4.8%.

West Vancouver: Total Units Sold in October were 59 – up from 45 (31%) in September, up from 57 (4%) in August, up from 53 (11%) in October 2023, up from 47 (25%) in October 2022, down from 90 (34%) in October 2021, down from 104 (43%) in October 2020, and down from 66 (11%) in October 2019; Active Listings were at 707 at month end compared to 609 at that time last year (up 16%) and 724 at the end of September (down 2%); the 213 New Listings in October were down 10% compared to September 2024, up 27% compared to October 2023, up 25% compared to October 2022, up 27% compared to October 2021, up 3% compared to October 2020, and down 7% compared to October 2019. Month’s supply of total residential listings is down to 12 month’s supply from 16 (buyer’s market conditions) and sales to listings ratio of 28% compared to 19% in September 2024, 32% in October 2023, and 27% in October 2022.

Month-over-month, the house price index is down 1.5% but in the last 6 months down 3.0%.

Richmond: Total Units Sold in October were 290 – up from 197 (47%) in September, up from 191 (52%) in August, up from 217 (34%) in October 2023, up from 243 (19%) in October 2022, down from 479 (39%) in October 2021, down from 384 (24%) in October 2020, and down from 345 (16%) in October 2019; Active Listings were at 1,657 at month end compared to 1,268 at that time last year (up 31%) and 1,736 at the end of September (down 5%); the 588 New Listings in October were down 7% compared to September 2024, up 22% compared to October 2023, up 29% compared to October 2022, up 9% compared to October 2021, down 6% compared to October 2020, and up 16% compared to October 2019. Month’s supply of total residential listings is down to 6 month’s supply from 9 (balanced market conditions) and sales to listings ratio of 49% compared to 31% in September 2024, 45% in October 2023, and 53% in October 2022.

Month-over-month, the house price index is down 1.4% and in the last 6 months down 3.7%.

Burnaby East: Total Units Sold in October were 25 – down from 29 (14%) in September, the same as August, up from 21 (19%) in October 2023, up from 22 (14%) in October 2022, down from 44 (43%) in October 2021, down from 50 (50%) in October 2020, and down from 26 (4%) in October 2019; Active Listings were at 158 at month end compared to 105 at that time last year (up 50%) and 148 at the end of September (down 7%); the 69 New Listings in October were up 3% compared to September 2024, up 44% compared to October 2023, up 97% compared to October 2022, up 109% compared to October 2021, up 11% compared to October 2020, and up 33% compared to October 2019. Month’s supply of total residential listings is up to 6 month’s supply from 5 (balanced market conditions) and sales to listings ratio of 36% compared to 43% in September 2024, 44% in October 2023, and 63% in October 2022.

Month-over-month, the house price index is flat% and in the last 6 months down 2.2%.

Burnaby North: Total Units Sold in October were 168 – up from 122 (38%) in September, up from 145 (16%) in August, up from 137 (23%) in October 2023, up from 96 (75%) in October 2022, down from 191 (12%) in October 2021, down from 170 (1%) in October 2020, and up from 166 (1%) in October 2019; Active Listings were at 791 at month end compared to 598 at that time last year (up 39%) and 839 at the end of September (down 6%); the 294 New Listings in October were down 13% compared to September 2024, up 1% compared to October 2023, up 46% compared to October 2022, up 56% compared to October 2021, up 4% compared to October 2020, and up 42% compared to October 2019. Month’s supply of total residential listings is down to 5 month’s supply from 7 (balanced market conditions) and sales to listings ratio of 57% compared to 36% in September 2024, 47% in October 2023, and 48% in October 2022.

Month-over-month, the house price index is down 0.4% and in the last 6 months down 2.6%.

Burnaby South: Total Units Sold in October were 166 – up from 114 (46%) in September, up from 112 (48%) in August, up from 120 (38%) in October 2023, up from 122 (36%) in October 2022, down from 228 (27%) in October 2021, down from 178 (7%) in October 2020, and up from 157 (6%) in October 2019; Active Listings were at 675 at month end compared to 515 at that time last year (up 31%) and 694 at the end of September (down 3%); the 285 New Listings in October were down 14% compared to September 2024, up 26% compared to October 2023, up 17% compared to October 2022, up 24% compared to October 2021, down 6% compared to October 2020, and up 23% compared to October 2019. Month’s supply of total residential listings is down to 6 month’s supply from 8 (balanced market conditions) and sales to listings ratio of 47% compared to 30% in September 2024, 42% in October 2023, and 47% in October 2022.

Month-over-month, the house price index is up 1.6% and in the last 6 months down 2.9%.

New Westminster: Total Units Sold in October were 120 – up from 73 (64%) in September, up from 79 (52%) in August, up from 81 (48%) in October 2023, up from 71 (69%) in October 2022, down from 166 (28%) in October 2021, down from 168 (29%) in October 2020, and down from 136 (12%) in October 2019; Active Listings were at 480 at month end compared to 305 at that time last year (up 57%) and 468 at the end of September (up 3%); the 255 New Listings in October were up 5% compared to September 2024, up 68% compared to October 2023, up 75% compared to October 2022, up 47% compared to October 2021, down 6% compared to October 2020, and up 59% compared to October 2019. Month’s supply of total residential listings is down to 4 month’s supply from 6 (seller’s market conditions) and sales to listings ratio of 47% compared to 30% in September 2024, 53% in October 2023, and 49% in October 2022.

Month-over-month, the house price index is down 2.1% and in the last 6 months down 2.3%.

Coquitlam: Total Units Sold in October were 246 – up from 155 (59%) in September, up from 171 (44%) in August, up from 167 (47%) in October 2023, up from 196 (26%) in October 2022, down from 303 (19%) in October 2021, down from 356 (31%) in October 2020, and down from 254 (3%) in October 2019; Active Listings were at 1,102 at month end compared to 778 at that time last year (up 42%) and 1,146 at the end of September (down 4%); the 468 New Listings in October were down 9% compared to September 2024, up 15% compared to October 2023, up 38% compared to October 2022, up 70% compared to October 2021, up 3% compared to October 2020, and up 41% compared to October 2019. Month’s supply of total residential listings is down to 4 month’s supply from 7 (seller’s market conditions) and sales to listings ratio of 53% compared to 30% in September 2024, 41% in October 2023, and 58% in October 2022.

Month-over-month, the house price index is down 0.8% and in the last 6 months down 4.0%.

Port Moody: Total Units Sold in October were 68 – up from 61 (11%) in September, up from 39 (74%) in August, up from 51 (33%) in October 2023, up from 44 (55%) in October 2022, down from 76 (11%) in October 2021, down from 92 (26%) in October 2020, and the same as October 2019; Active Listings were at 253 at month end compared to 170 at that time last year (up 49%) and 251 at the end of September (up 1%); the 146 New Listings in October were up 2% compared to September 2024, up 72% compared to October 2023, up 80% compared to October 2022, up 106% compared to October 2021, up 19% compared to October 2020, and up 78% compared to October 2019. Month’s supply of total residential listings is steady at 4 month’s supply (seller’s market conditions) and sales to listings ratio of 45% compared to 43% in September 2024, 60% in October 2023, and 54% in October 2022.

Month-over-month, the house price index is down 3.1% and in the last 6 months down 2.2%.

Port Coquitlam: Total Units Sold in October were 77 – up from 52 (48%) in September, up from 56 (38%) in August, up from 54 (43%) in October 2023, up from 62 (24%) in October 2022, down from 120 (36%) in October 2021, down from 122 (37%) in October 2020, and down from 107 (28%) in October 2019; Active Listings were at 328 at month end compared to 201 at that time last year (up 63%) and 358 at the end of September (down 8%); the 148 New Listings in October were down 20% compared to September 2024, up 30% compared to October 2023, up 21% compared to October 2022, up 13% compared to October 2021, down 16% compared to October 2020, and up 16% compared to October 2019. Month’s supply of total residential listings is down to 4 month’s supply from 7 (seller’s market conditions) and sales to listings ratio of 52% compared to 28% in September 2024, 47% in October 2023, and 51% in October 2022.

Month-over-month, the house price index is up 0.8% and in the last 6 months down 2.2%.

Pitt Meadows: Total Units Sold in October were 32 – up from 24 (33%) in September, up from 21 (52%) in August, up from 21 (52%) in October 2023, up from 21 (52%) in October 2022, down from 34 (6%) in October 2021, down from 39 (18%) in October 2020, and up from 31 (3%) in October 2019; Active Listings were at 121 at month end compared to 91 at that time last year (up 32%) and 125 at the end of September (down 3%); the 57 New Listings in October were down 19% compared to September 2024, up 21% compared to October 2023, up 39% compared to October 2022, up 78% compared to October 2021, up 16% compared to October 2020, and up 19% compared to October 2019. Month’s supply of total residential listings is down to 4 month’s supply from 5 (seller’s market conditions) and sales to listings ratio of 56% compared to 34% in September 2024, 44% in October 2023, and 51% in October 2022.

Month-over-month, the house price index is up 3.6% and in the last 6 months down 0.7%.

Maple Ridge: Total Units Sold in October were 143 – up from 114 (25%) in September, up from 123 (16%) in August, up from 110 (30%) in October 2023, up from 99 (44%) in October 2022, down from 187 (24%) in October 2021, down from 293 (51%) in October 2020, and down from 180 (21%) in October 2019; Active Listings were at 848 at month end compared to 774 at that time last year (up 9%) and 887 at the end of September (down 4%); the 316 New Listings in October were down 8% compared to September 2024, down 4% compared to October 2023, up 37% compared to October 2022, up 85% compared to October 2021, up 9% compared to October 2020, and up 31% compared to October 2019. Month’s supply of total residential listings is down to 8 month’s supply from 6 (balanced market conditions) and sales to listings ratio of 45% compared to 33% in September 2024, 33% in October 2023, and 42% in October 2022.

Month-over-month, the house price index is flat and in the last 6 months down 1.7%.

Ladner: Total Units Sold in October were 31 – up from 22 (41%) in September, up from 25 (24%) in August, up from 24 (29%) in October 2023, up from 21 (48%) in October 2022, down from 38 (18%) in October 2021, down from 55 (44%) in October 2020, and up from 21 (48%) in October 2019; Active Listings were at 142 at month end compared to 119 at that time last year (up 19%) and 136 at the end of September (down 4%); the 61 New Listings in October were down 16% compared to September 2024, up 39% compared to October 2023, up 56% compared to October 2022, up 22% compared to October 2021, up 20% compared to October 2020, and down 8% compared to October 2019. Month’s supply of total residential listings is down to 5 month’s supply from 6 (balanced market conditions) and sales to listings ratio of 51% compared to 30% in September 2024, 55% in October 2023, and 57% in October 2022.

Month-over-month, the house price index is down 0.8% and in the last 6 months down 1.0%.

Tsawwassen: Total Units Sold in October were 36 – up from 34(6%) in September, up from 32 (13%) in August, up from 27 (33%) in October 2023, up from 28 (29%) in October 2022, down from 64 (56%) in October 2021, down from 76 (53%) in October 2020, and up from 32 (13%) in October 2019; Active Listings were at 223 at month end compared to 188 at that time last year (up 19%) and 215 at the end of September (up 4%); the 80 New Listings in October were the same as September 2024, up 7% compared to October 2023, up 29% compared to October 2022, up 40% compared to October 2021, down 6% compared to October 2020, and down 1% compared to October 2019. Month’s supply of total residential listings is steady at 6 month’s supply (balanced market conditions) and sales to listings ratio of 45% compared to 43% in September 2024, 36% in October 2023, and 45% in October 2022.

Month-over-month, the house price index is down 3.1% and in the last 6 months down 7.4%.

Fraser Valley: Sales in October were down 35.4%, compared to September and were up 37.1% from October 2023. New listings were down 4.7% from September and up 26.0% from October 2023.The average price was down 0.8% month-over-month and is up 2.3% year-over-year. Active listings were down 2.7% to 8,799 from 9,045 last month and up 33.7% from October 2023 which was at 6,580. Month’s supply of total residential listings is down to 7 month’s supply from 9 (balanced market conditions).

“After waiting it out on the sidelines for a number of months, buyers seem to be finally responding to the series of successive rate cuts by the Bank of Canada,” said Jeff Chadha, Chair of the Fraser Valley Real Estate Board. “Whether this is an indication of further sales trends, remains to be seen, especially as the feds eye a possible additional cut before year-end.”

Month-over-month, the house price index is down 3.8% and in the last 6 months 3.5%.