Highlights of Dexter Realty’s February 2023 Report

Prices increased month-over-month for the first time since May 2022

Housing sales are up 77% from January; new listings are up just 5%.

Multiple offers are being seen on Westside detached houses.

Top townhouse market: New Westminster.

Undersupplied North Vancouver is now a seller’s market.

The last three years have been an anomaly for housing markets around the world and Greater Vancouver is no exception. That is why it is virtually useless to compare our current, back-to-reality environment with what was happening a year or two years ago during a once-in-a-century event.

In 2021, we were in the grip of a global pandemic and a home-buying frenzy with mortgage rates at record lows. In February 2022, housing sales and prices hit a white-hot peak just before the federal government hosed it down with the first of eight straight interest rate increases through the Bank of Canada.

Today, in February 2023, the panic buying is history, mortgage rates have stabilized, and buyers are back into the first normal housing market in four years. Driven by buyer demand and low supply, February marked the first month-to-month home price increase in nine months.

Greater Vancouver housing sales, at 1,824 transactions in February, were up 77% from January 2023 and 21% higher than in February 2019, before the whole pandemic-influenced housing boom-and-bust began. February sales were also higher than in November and December 2022, and, we believe, signal the start of a strong spring selling season.

Buyers are already competing with other buyers for far fewer listings. The number of new listings in February was the lowest for that month going back to pre-1991, much the same as it was in January. Compared to January 2023, listings were only up 5%.

But, since sales have been slower over the past 10 months, a total of 8,283 homes were on the market at the of February, above the 7,862 active listings at the end of January and a few hundred more than in December 2022.

With buyers flowing back into the market, immigration hitting record levels and interest rates settling down, this appears a prime time to encourage housing starts. However, governments at all levels appear to be doing their best to stunt new home construction.

The federal government has banned foreign buyers for two years, including those investing in residential land, if the developer has less than 97% Canadian ownership. For example, a 3,000-unit Burnaby residential development, now under construction, would not be allowed today because the developer is based out of London, England. The recent collapse of major condo developers in Metro Vancouver could be traced to the ban’s impact on companies with as little as a 3% foreign ownership. This has put thousands of new homes at risk.

The B.C. government is spending $500 million to stop or stall the private redevelopment of 50 and 60-year-old rental buildings into modern, higher-density housing projects.

Metro municipalities are jacking up development cost charges, even as housing starts fall. Among the examples is Richmond, where housing starts so far in 2023 total just 73 units, down 80% from the 381 starts at the same time a year ago. Richmond is raising DCC rates on single-family lots by $20,000 to $61,138, and raising the DCC rate for condo apartments and townhouses by 43% to more than $34 per square foot. This means that a modest new townhouse of 1,200 square feet will now cost about $41,000 just in city development fees.

All governments preach about addressing the supply of ‘missing middle’ housing for families, which translates as townhouses. Yet only 3 townhouse units have started so far this year in the City of Vancouver, compared to just 21 units a year ago at this time – and a mere 90 townhouse units were started in all of 2022 across Metro Vancouver.

For residential investors, the consistent housing shortage is a blessing, which is why Metro Vancouver has become a “buy and hold” housing environment. Owners know that the law of supply and demand ensures that home prices will keep increasing. So they wait it out. In markets where sales levels are declining, an increase in new listings would add to the active listing count and provide downward pressure on prices.

That’s not the Metro Vancouver market, where sales are turning back up.

Any increase in new listings will be absorbed by buyers. With the level of competition we are now seeing in the market, buyers are craving listings and competing for different product types in different areas. Active listing counts are up about 500 since the end of December. Absorption rates today are twice what they were in a similar market in 2019, and are only held in check by the lack of homes on the market.

The bottom line: Greater Vancouver listings are scarce at a time when they should be double what they are.

Prior to 2015, having 15,000 to 20,000 active listings in Greater Vancouver was the norm. Since then, we’ve barely scratched above 15,000 and right now we are at half that level. Restrictive zoning and slow-moving development approvals continue to barricade supply. And without that supply, a seller’s markets will continue, at whatever level of demand we have in the market.

A look at the Regional housing numbers:

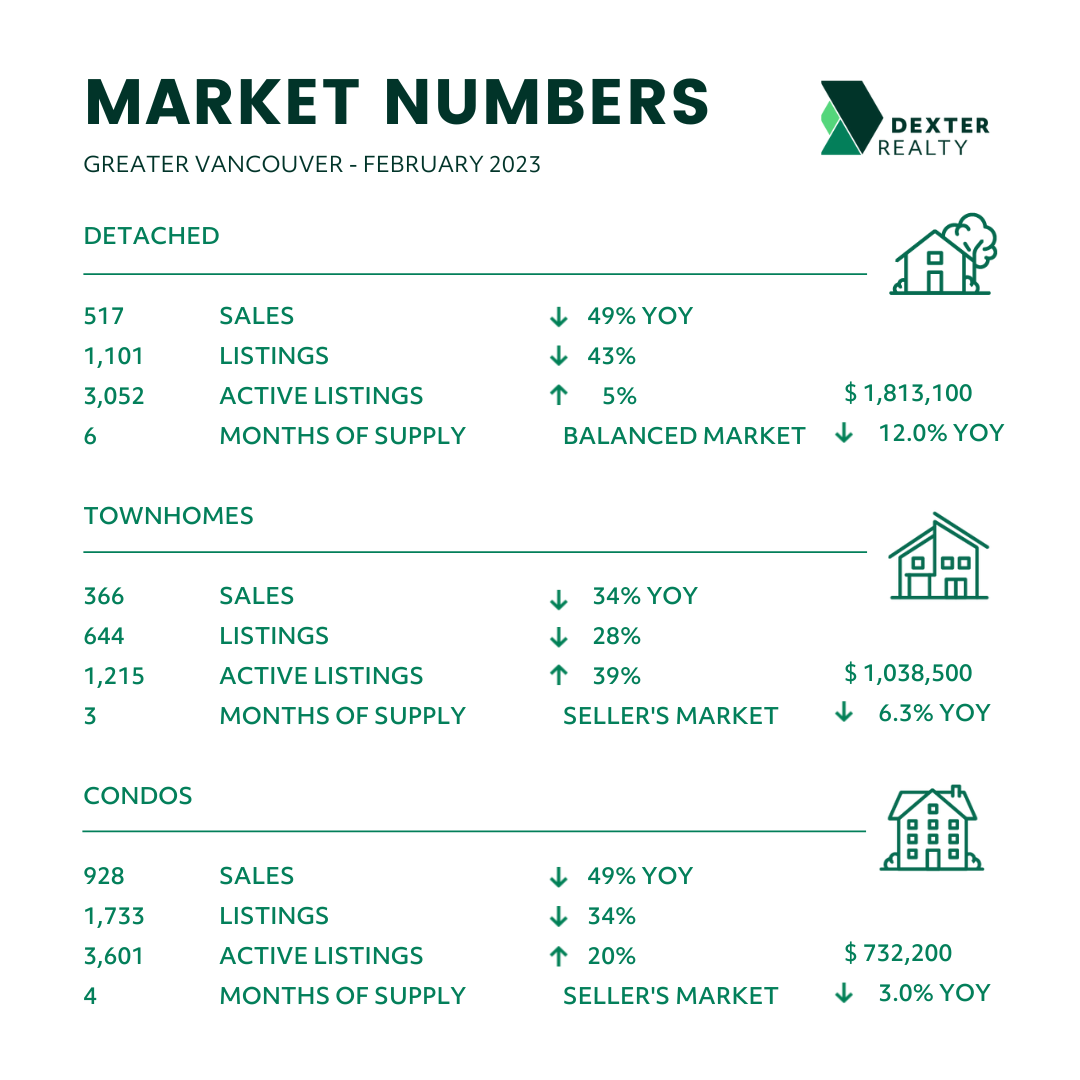

Greater Vancouver: Total housing sales were up 77% compared to January 2023, while new listings were up 5%. The result was the composite benchmark home price posted the first month-over-month increase since May of 2022, rising 1.1% to $1,123,400. Detached house prices rose 0.7%, to $1,813,000; condo apartment prices rose 1.6% to $732,200; and townhouse benchmark prices were up 1.8%, compared to a month earlier, to $1,038,500. Active Listings were at 8,283 at month-end compared to 7,062 at that time last year and 7,862 at the end of January. Greater Vancouver’s detached housing market is now seen as a balanced market, with both condo apartments and townhouses in a seller’s market. The total sales-to-new-listing ratio in February was 51%, compared to 30% in January 2023 and 62% in February 2022.

Fraser Valley: The Fraser Valley Real Estate Board processed 898 sales in February, an increase of 43.5% over January 2023, but still only half as many as were recorded a year ago. February new listings were up by 5.7% over January 2023 to 1,938 but 48.25% lower than in February 2023. Active listings were up 7% from a month earlier. The composite benchmark home price in February was $946,700 up 0.5% from January 2023 and the first month-over-month increase since April 2022. Further, the benchmark price is 36% higher than in pre-pandemic February 2020.

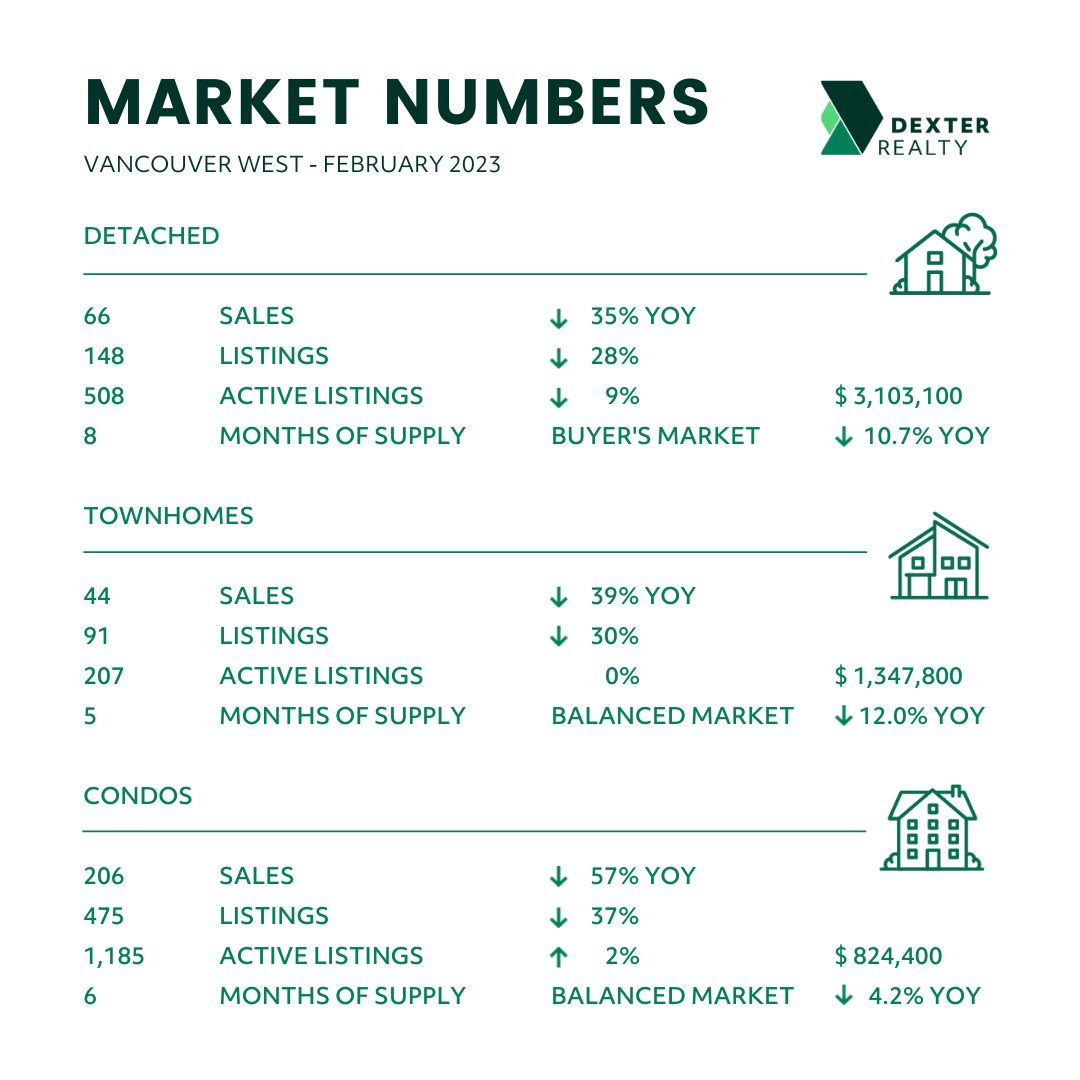

Vancouver Westside: February total sales, at 316, were up 63% from January 2023 and would have been even higher if more listings were available. One Westside house had 16 offers on it at the end of February, an indication of the demand. New listings were down 1% from January, but active listings as of month end were at 1,923, representing about a six-month supply. The sales-to-new-listing ratio is running at 44%, up from 27% a month earlier. There is a severe shortage of townhouses, with nearly half the 91 new listings selling in February at a median price of more than $1.48 million. No new townhouses have started construction this year on the Westside. The February benchmark price for a detached house on the Westside jumped 2.7% from a month earlier, to $3,103,100.

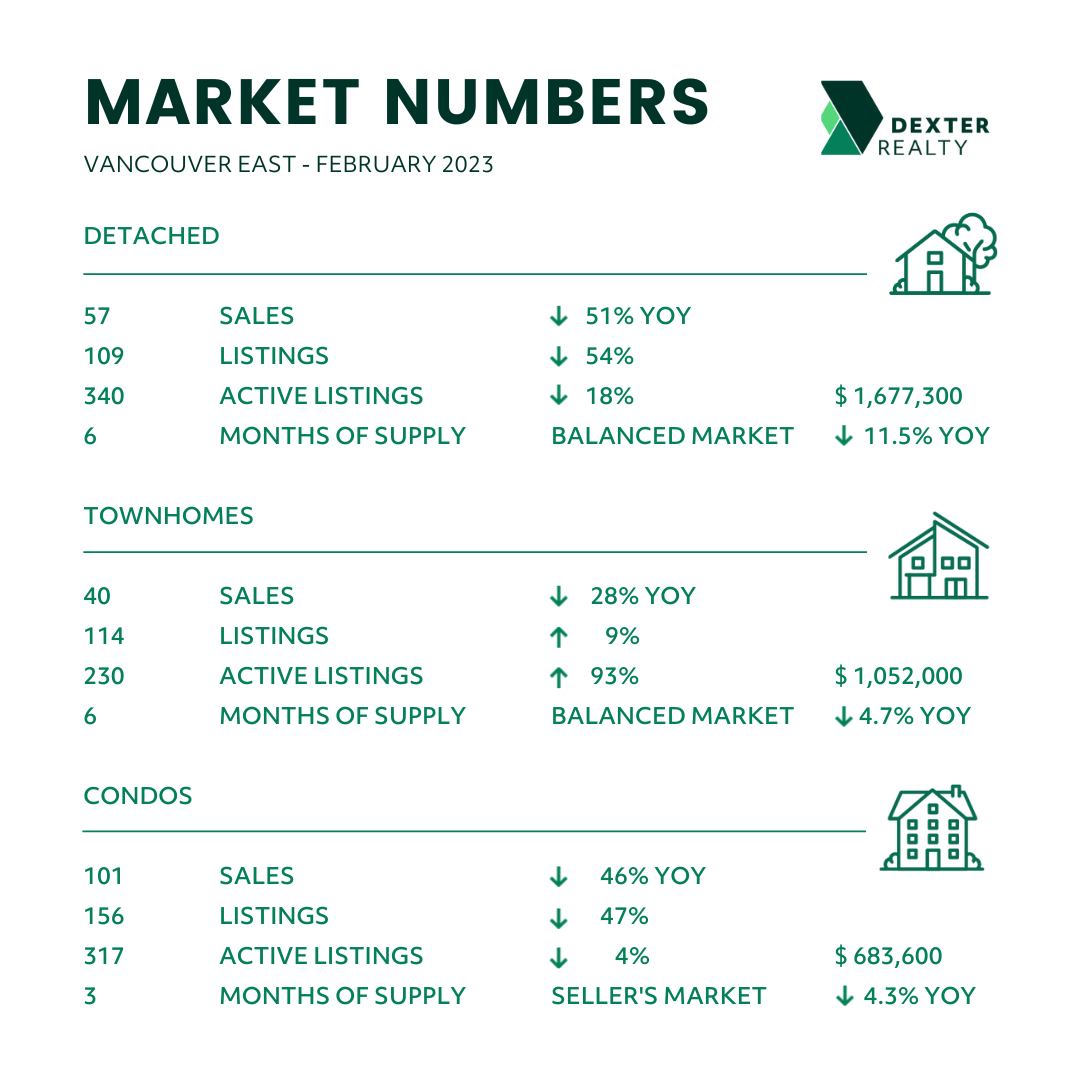

Vancouver East Side: Total housing sales in February, at 198, were up 68% from January 2023, but new listings were up by only 6%, while the sales-to-new-listing ratio reached a balanced 52%, up from 33% in January, and close to 55% ratio in the hot market a year ago. This is a market to watch. Benchmark prices were up in all sectors from a month earlier, led by a 2.9% surge in townhouse prices to $1,052,500. The supply of total residential listings is down to five months supply, with condos in seller’s market conditions. Benchmark condo prices were up 1% from January, to $683,600, based on 101 sales, double the number a month earlier.

North Vancouver: This perpetually under supplied market is a seller’s market with only a three-months supply of listings, even with growth in active listings of townhouses and condos. A total of 150 sales were seen in February, up 83% from a month earlier, but active listings were just 20 homes higher, at 436 units. With the sales-to-listing ratio at 59%, townhouse prices shot up 4.1% from January 2023, to $1,286200, and detached and condo benchmark prices were up nearly 2% from a month earlier.

West Vancouver: Sales increased 54%, month over month to 43 transactions, but because of a 21% spike in new listings, there is now a 10-month supply of homes, in this buyer’s market for detached houses. It remains a seller’s market for townhomes, because the supply is so low, perhaps one reason West Vancouver’s population is declining. West Van posted a modest decline in most prices compared to January, except for condo apartments, which were up 2.7% to a region-leading $1,228,900.

Richmond: Despite the angst in Richmond’s strata market – where an 800-unit development has gone into receivership and starts have plunged 80% from a year ago, total sales in February were up 89% from January. The benchmark composite home prices rose 2% from a month earlier with condos selling for $735,800; townhouses at $1,083,100; and detached houses at just over $2 million. With an overall sales-to-listing ratio of nearly 50%, the detached-house market is in balanced conditions, with a seller’s market building steam in the strata sector.

Burnaby East: Total sales in February were 21, up 133% from a month earlier and the sales-to-listing ratio hit a stunning 105%, compared to a low of 20% in January 2023 and 52% in February of last year. This is a seller’s market on steroids with the composite benchmark price up 2.2% month-over-month to $1,102,900, the highest in Burnaby.

Burnaby North: With total sales up 113% from January 2023, to 134, and total active listings down 10%, this is also a seller’s market with a mere three-month supply of listings and a sales ratio of 66%. The saving grace is the high number of new condos coming to the market in the Brentwood-Gilmore area. The composite home price was up from January, led by a 2.4% surge in townhouse prices to $892,100.

Burnaby South: Many Burnaby buyers were southbound in February, driving total sales up 119% from a month earlier, to 118 transactions. Active listings were 377 at month end compared to 352 at the end of January, which translates to a three-month supply at the current sales pace. The composite benchmark price was up nearly 1% from January at $966,500. The sales-to-listing ratio is a healthy 57% with the strata sector in seller’s market conditions.

New Westminster: For buyers looking for scarce townhouses, the Royal City has a good selection. Only 3 townhouses sold in February and there is nine-month supply on the market. Benchmark townhouse prices, however, increased 4.4% from January 2023, to $932,200, the same price as in February 2023. Total housing sales in February were 65% higher than a month earlier, at 66, at new listings inched up by 1%. The overall sales-to-listing ratio is 62%, up from 38% in January 2023 with a buyer’s market for townhouse and condos and a balanced market for detached houses, where prices are up 2.4% or about $34,000 – from a month earlier at $1,418,100.

Coquitlam: It seems hard to understand with the amount of new multi-family construction over the past two years, but Coquitlam is seeing a shortage of strata homes. Coquitlam had one of the biggest turnarounds in February with sales up 116% compared to January. Townhouse sales went from 4 in January to 40 in February. With that, there is just a two-months of inventory for townhouses and condos. The composite benchmark price is up 0.7% from a month earlier, but townhouse prices rose 2.5% from January to $999,900. With an overall sales-to-listing ratio of 67%, this is a seller’s market for strata units and balanced in the detached sector.

Port Moody: Even with total listings of 200 at the end of February, and a significant increase in townhouse and condo listings, strata units are in a seller’s market, along with detached houses. There were more sales than new listings compared to January, with a 104% sales increase from the month previous, to 47 transactions while only 91 new listings in February compared to 103 in January. More than half (52%) of the new listings sold in February, while the composite benchmark price increased 1% to $1,093,100, the highest in the Tri-Cities.

Port Coquitlam: There is only a one-month supply of townhouses with twice as many sales as new listings in February. Total housing sales reached 40, up a modest 18% from January 2023. The total supply of residential listings is down to four months, meaning a balanced market conditions for detached houses, with townhouses and condos in seller’s market conditions. The overall sales-to-listing ratio is a healthy 46% and the composite benchmark price has held steady (up 0.7%) for three months at $900,900.

Pitt Meadows: Sales didn’t budge month-over-month, with 15 transactions in February, while new listings fell 29% compared to January 2023. The total inventory remains at a four-month supply in this balanced market, with a sales-to-listing ratio of 55%. The composite benchmark home price fell 0.6% from January to $825,900.

Maple Ridge: Total housing sales in February were up 98% from January 2023 to 129 transactions, but new listings were down 4% from a month earlier. With a sales-to-listing ratio of 62%, the same as in February of last year and up from 30% in January 2023, this is a sellers’ market with just four months of inventory. Still, Maple Ridge plans to increase development cost charges this year to $41,000 for a new detached house, up from $22,465, and raise per-square-foot fees for new condo and townhouse units by 80%. The composite benchmark home price in February was up about 1% from January, at $918,300, but townhouse prices rose 3.5%, month over month, to $723,600.

Ladner: The townhouses market saw significant increases in sales and listings accounting for as many sales in February as detached and condos combined. Still, the total market was fairly brisk, with 27 transactions, up 69% from a month earlier and higher even than in February of last year. Townhouse prices spiked up 6.7% from January 2023 tied as the highest increase in Metro Vancouver – to $988,600. New listings were up 42% from a month earlier and there were 98 active listings as February ended. With a sales-to-listing ratio of 44%, this is a balanced market slanting towards a seller’s advantage for townhouses and condos.

Tsawwassen: Detached house listings were down 41% compared to January, while condos remain with a three-month supply. Detached houses and townhouses are in a balanced market. Total sales were rather tepid, at 25 transactions compared with 20 in January 2023 and 73 in February 2022. Perhaps buyers are tired of the back-and-forth Massey Tunnel replacement plan that doesn’t seem to ever get off (or under) the ground. This was noticeably absent from the recent provincial budget announcement and its three-year infrastructure plans. Despite a sales ratio of 47%, the composite benchmark price was down 3.7%, month-over-month, to $1,112,800, led by a sharp 7% drop in detached house prices.

Surrey: Benchmark home prices in Surrey were higher than in January, the first month-over-month increase since April of 2022. Detached house prices were up 0.7% to $1,503,200; townhouse prices rose 1% to $ $ 803,100 and condo apartment benchmark prices were up 1.4% to $522,700. The outlier is South Surrey-White Rock’s detached market, where prices slipped down 1.4% from January to $1,776,300, still the highest price in the Fraser Valley. With total Surrey sales up 61% from January 2023, at 132 transactions, and new listings up less than 15%, Surrey is considered a balanced market.

Download February Sales and Listings Statistics Houses Townhouses Condos

Download February Sales and Listings Statistics All Regional