“Inaction breeds doubt and fear. Action breeds confidence and courage. If you want to conquer fear, do not sit home and think about it. Go out and get busy.“

Dale Carnegie

Homebuyers, investors take advantage in this market

Highlights of the July Report

- Average 5-year mortgage rates are up just 1.4% from six months ago.

- First-time homebuyers in B.C. are down 46% compared to a year ago.

- Foreign homebuyers now account for just 1% of Metro transactions.

- July benchmark detached house price is up $47,500 from January 2022.

- The number of active listings are in decline

There are two sectors of homebuyers in Metro Vancouver’s market: owner-occupiers buying for their own use and investors buying homes for rental income or appreciation, with the latter traditionally accounting for about 20% of transactions. The current calming of the housing market represents an historical opportunity for both parties.

The current calming of the housing market represents an historical opportunity for both parties. For homebuyers who plan to purchase a property to live in for a long time, the current hysteria over rather modest mortgage interest rate hikes shouldn’t impact their purchase decision. After the drama of three Bank of Canada rates hikes, the average five-year fixed-rate mortgage at Canada’s six big banks has increased by just 1.4% in the last six months. Buyers purchasing into a five- or 10-year ownership horizon will be glad they bought during this lull in the summer of 2022.

It is rather ironic that, as strong economy creates near full employment in B.C. some look back to the global pandemic as the good old days.

But those who bought a Greater Vancouver home in pre-pandemic July 2019 – when the market was quite sluggish – would have experienced an average lift in benchmark value of 21% as of this month, or a cash increase in excess of $212,000. A detached house returned 41%, or a typical increase of $583,600, despite the recent easing of detached prices.

Since the start of this year, the typical detached house price is up by $47,500, though prices have declined over the past four months.

Of course, there is the psychological, counterintuitive factor at play, as many homebuyers pull to the sidelines just when they should be buying and then plunge in just when the market is peaking. It is a consistent phenomena that defies logic or change. The winning homebuyers in the current market cycle, as in the sleepy summer of 2019, will be those who act while others hesitate.

Some buyers, however, are being shunted aside in the current cycle: first-time homebuyers and foreign buyers. This may prove a boon to investors.

During the first half of this year, the number of B.C. first-time buyers fell 46% compared to the same period last year, accounting for just 4,426 purchasers. A key reason is the federal government’s mandatory stress test, which requires buyers to qualify at an unrealistically high five-year mortgage rate that many first buyers have difficulty meeting. Instead of buying, more than 4,000 will remain renters.

Also, while foreign homebuyers before the Foreign Buyer Tax may have accounted for 6% or more of all sales, they now make up only 1% of Metro Vancouver transactions, according to the BC Finance Ministry. The reason is a 20% of a home’s value tax on foreign buyer and the looming two-year ban on foreign homebuyers next January by the Federal Government.

So, investors who are purchasing investment condominiums now are enjoying lower prices, zero competition from global investors, a captive audience of renters and rising rental rates.

Investors realize that, despite all the government chest thumping over increasing the supply, Metro Vancouver housing starts as of July were down 23% from a year earlier and the new strata shortage is getting worse.

Part of the reason for this is government fees and taxes on new condos and townhomes, which, according to a survey released July 5 by Canada Mortgage and Housing Corp., account for up to 20% of a new strata price in Metro Vancouver. The Government Charges on Residential Development in Canada’s Largest Metropolitan Areas survey found a typical developer’s profit on a new condo is estimated at between 10% to 15%, so Metro Vancouver municipalities can make more money on a new home than those who build it. That’s not right, but it is reality.

The City of Vancouver, CMHC reported, has Canada’s highest average cost per-square-foot on new strata buildings, at $143 per square foot, owing entirely to density payments.

When the market was surging, private developers could handle such disparity. With sales and prices slowing, projects are being delayed or cancelled, which will lead to a further shortage of new condos and townhouses this fall.

We are now in a brief and government-induced buyer’s market that both homebuyers and savvy investors should take advantage of. While the market is slower now, like every market, this one will turn too. Buyers, enjoy it now!

Here is a look at the regional numbers:

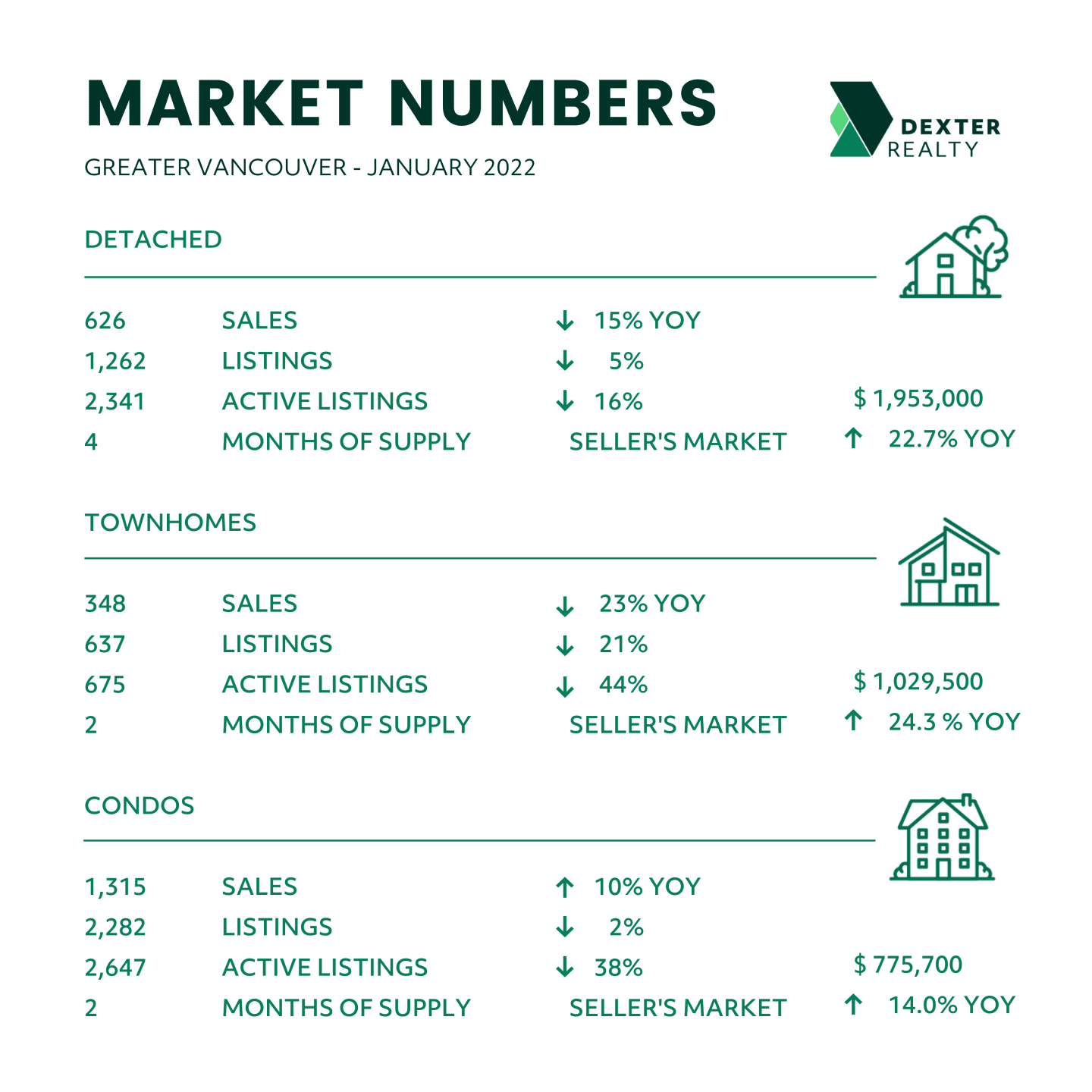

Greater Vancouver: With the total inventory of homes for sale now at 6-month supply, the market has moved into balanced territory with some regions into a buyer’s market, especially for detached houses. The sales-to-listing ratio for detached houses in July fell to 39% and there are 8-months supply of homes available, which, if it persists, generally means prices are heading lower. A total of 1,904 residential properties sold in July, down 33% from a month earlier and 44% lower than in July 2021 and lower than even July 2019 and 2018. The composite benchmark home price in July is $1,207,400. This is a 10.3% increase over July 2021 but a 2.3% decrease compared to June 2022. Benchmark prices have been slowly declining, month-over-month since February. The July benchmark price for a detached home is $2,000,600, a 2.8 per cent decrease compared to June 2022. Active listings were at 10,734 at month end compared to 10,367 at that time last year but nearly unchanged from June 2022 at 10,839; New listings in July were down 25% compared to June 2022 and 10% lower than in July 2021.

July saw 4,067 new listings come to the market which was below the 5,410 that came on the market in June 2022 and less than the 4,514 that came out in July 2021 – sellers are beginning to hold off as well as many aren’t prepared to sell at prices below what they could have obtained earlier this year. And with less, listings, there are more properties coming off the market that were listed which is resulting in lower active listing counts. The number of new listings in July were 19% below the 10-year average (down from 3.5% below the 10-year average last month).

Fraser Valley: In July, the Fraser Valley Real Estate Board reported 993 sales, a decrease of 22.5% from the previous month and a 50.5% drop compared to July 2021. July new listings totalled 2,385, down 28.4% compared to June 2022 and a decrease of 1.9% from July 2021. Active listings, at 6,413, were unchanged from June and up 30.9% over last July – bringing the sector into balance for townhomes and detached homes (sales-to-active ratios: 18% and 12% respectively); and favouring sellers slightly for apartments. Benchmark prices dropped for the fourth consecutive month, most notably for detached homes which ended the month with a benchmark price of $1,594,400, down 10.2% since peaking in March 2022. Residential combined properties benchmark prices are up year-over-year by 18.1 per cent. Clearly the biggest gain earlier this year is seeing more of a pull back.

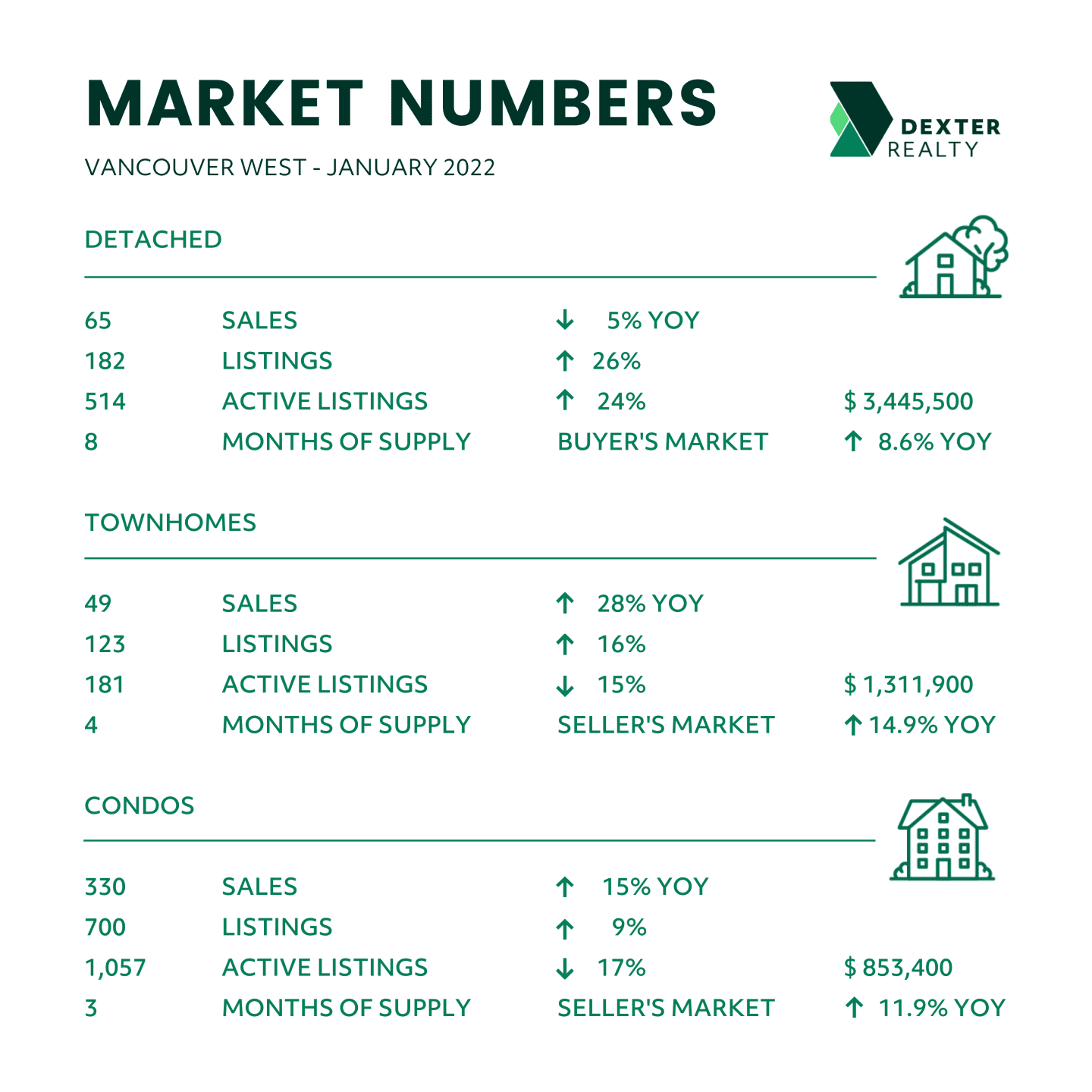

Vancouver Westside: There were only 368 total residential sales in July, down 18% from a month earlier to the lowest July level in at least four years. The Westside now has a 15-month supply of detached houses on the market, signally a buyer’s market in this sector. The July benchmark price of the 43 detached house sales was down 3.4% from June 2022 to $3,381,800. That is a drop of about $115,000 in a single month. Total active listings were 2,453 at month end compared to 2,558 at that time last year and down 3% from June 2022. New listings in July were down 23% compared to June 2022 and lowest level since at least July 2019. Condominiums now dominate the Westside, accounting for 294 sales in July at a benchmark price of $844,300.

Vancouver East Side: As the Broadway subway, the new St. Paul’s Hospital medical campus and a growing tech sector take shape in the area, the East Side could be the right side for investors this year. The median price of the 101 detached house sales sold in July was $1,790,000, almost exactly half the house price on the Westside. The East Side is a rare market where developers continue to assemble residential lots for higher-density strata (there are at least six land assemblies underway) and rentals. The July sales-to-listing ratio for detached houses was 39%, with condo sales ratios at 53%. With 1,191 total active listings and just 198 sales in July, there is an opportunity to find very good investments amid a healthy inventory. Look to the East 12th and Renfrew area and Commercial Drive to Main Street for condo rental and detached-house investor opportunities. The inventory of total residential listings is up to 6 month’s supply in a market seeking balance but favouring sellers.

North Vancouver: North Vancouver appears to have lot of construction underway, but nearly all the apartment starts this year are rentals, including 536 of the 750 new apartments. Actually, new strata starts are at near record lows. This is a concern, because new listings were down 35% in July compared to a month earlier and the total inventory of homes for sale is at just 573, while the sales ratio was running at 57%, up from 43% in June 2022. In July, 44 houses sold at a median price of just over $2 million, virtually unchanged from June but up $125,000 from a year earlier. With only a 3-month supply of listings on the market and steady prices, North Vancouver remains a seller’s market.

West Vancouver: With 30 of the total 43 sales in July, detached houses remain the draw for buyers in Metro’s most exclusive community. The benchmark price of a detached house in West Vancouver dropped 3.3% in July from a month earlier, yet remained at $3,376,200, second highest behind the Westside. Condo prices in West Vancouver, however, posted the biggest price drop – 6% – in Metro over the past three months, to $1,243,300. With total July sales down from a month and a year earlier and the inventory up to a 12-month supply, a mild buyer’s market is emerging in this aspirational market.

Richmond: Perhaps no other Metro market will feel the sting of a two-year foreign homebuyer ban as much as multicultural Richmond. The ban is to begin January 1, 2023, though surveys show that foreign-home buyers now account for only 1% of transactions. The ban has notable exemptions for permanent residents and temporary residents, including temporary workers and international students. Still, Richmond sales were down 44% in July from June 2022 and 48% lower than in July of last year, to just 223 transactions. The composite benchmark price is $1,162,400 after declining 3.2% over the last three months. Active listings were at 1,356 at month end compared to 1,380 at the end of June 2022. Total supply of residential listings is up to 6-month’s supply, which signals a balanced market, and the sales-to-listing rate is a very balanced 52%. Richmond could go either way, but we believe it could tilt into a buyer’s market this fall.

Burnaby East: Burnaby East is a fine family neighbourhood with two large parks, good schools, transit and shopping but it was looked over by buyers in July. Total housing sales were just 22, down 52% from a year earlier to the lowest monthly level this year. However, with a very tight supply – just 68 total listings – new listings down 42% from a year ago and a sales-to-listing ratio of 67%, this remains a seller’s market. Composite prices have been dropping for three months and were down 2.1% from June 2022 at $1,154,200; detached house have declined to $1,805,400, the lowest in Burnaby.

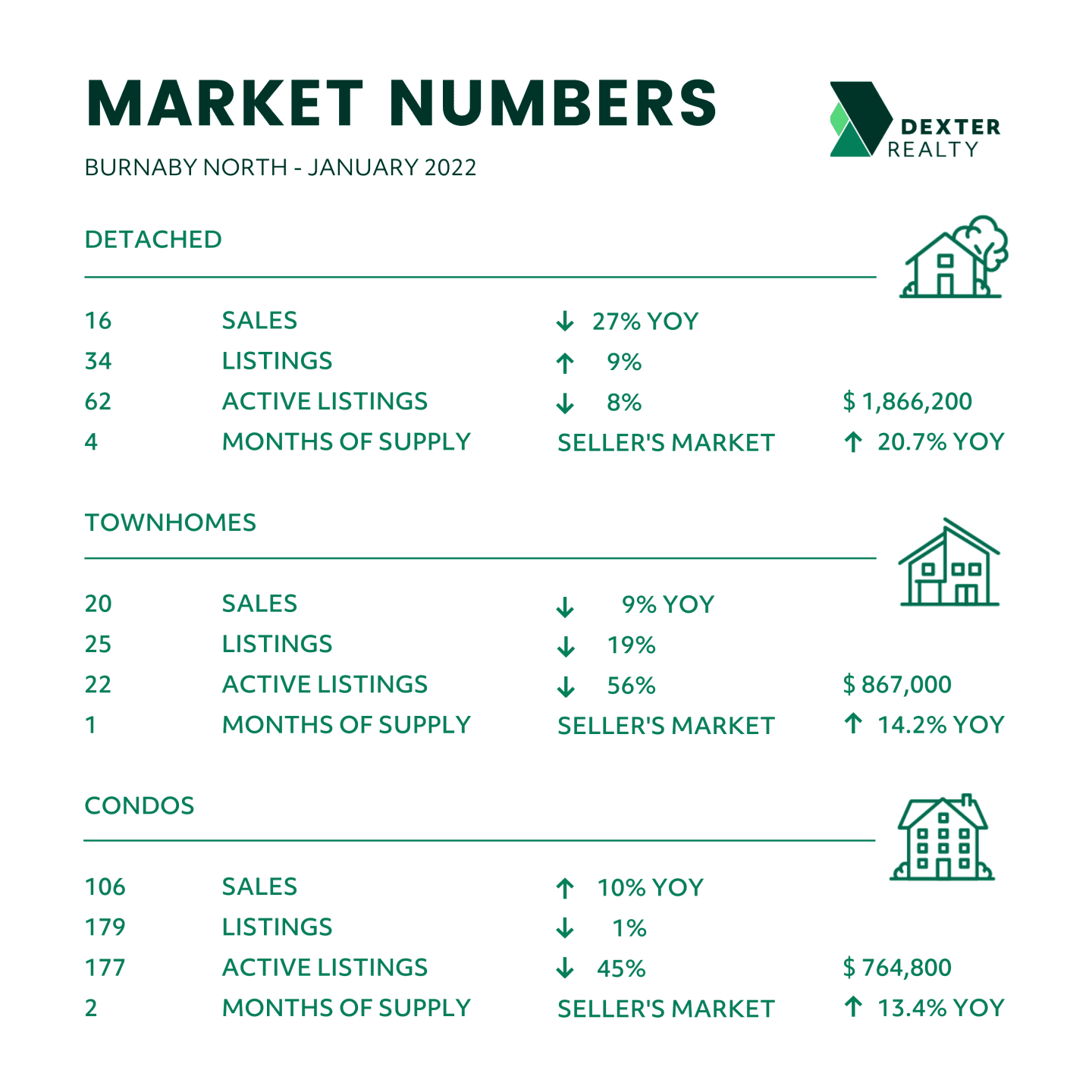

Burnaby North: With U.K.-based Grosvenor proceeding with a 7.9-acre land assembly in Brentwood for a “car-free” high-density rental and condo development, and Shape Properties marketing its sixth tower in the area, high-rise condos will continue to define Burnaby North. In July, the benchmark condo price was unchanged from June 2022 at $734,800, but 15% higher than a year earlier. The biggest price drop has been in townhouses, which shed 4% from June 2022 to a $942,600 benchmark. Total housing sales, at 124, were down 37% from a year earlier and lower than in both May and June of this year. Despite the surging condo construction, there is only a total inventory of 4 month’s supply of total listings and the sales-to-listing ratio is holding steady at 51%. This is seller’s market, with slightly lower prices.

Burnaby South: With the sales-to-listing ratio at 61% in July, local buyers may be surprised that sales were down 12% from a month earlier and 38% below July 2021, at 126 transactions. Yet, prices are also down, posting the biggest drops in Burnaby this year. Detached house prices are down 7.2% from June 2022, at $2,108,600; townhouse prices are down nearly 5% at $990,500. July condominium benchmark prices were off 3.2% from three months earlier, at $778,600. New Listings in July were down 27% compared to June 2022 and 24% lower compared to July 2021. This is technically a seller’s market but it is leaning towards a buyer’s price advantage.

New Westminster: The July composite home benchmark price in the Royal City was $834,200 after falling 3.7% since April to the lowest price in Greater Vancouver, below even Maple Ridge and the Sunshine Coast, both of which are much further from Vancouver’s SkyTrain network. A detached house in New Westminster is now benchmarked at $1,487,200, down 8.2% from three months earlier. Condo apartment prices are holding steady at $661,500 as are townhouses, down just 0.7% from June 2020 at $945,300.

Total July sales reached 82 transactions, down 50% from a year earlier and 26% below June 2020. Total inventory is 293 listings, which equates to about a 4-month supply at the current sales pace, which is posting a sales-to-listing ratio of 55%. Buyers may find some lower-priced deals in New Westminster this summer, but we expect the market to firm in September.

Coquitlam: Total housing sales have cooled sharply, dropping 25% in July from a month earlier and down 51% from a year earlier. Blame it on the summer heat, perhaps, but new listings are also fading, down 23% from June. The sales ratio is sitting at 50% and there is about a 5-month supply of active listings in what has become a balanced market. Benchmark prices for detached houses have fallen 5.5% since April to $1,853,500. Townhouse prices have been dropping 2% per month since March to reach $1,080,700 in July. Half of the new listings sold in July and we expect family-friendly Coquitlam home sales to pick up after kids are back in school.

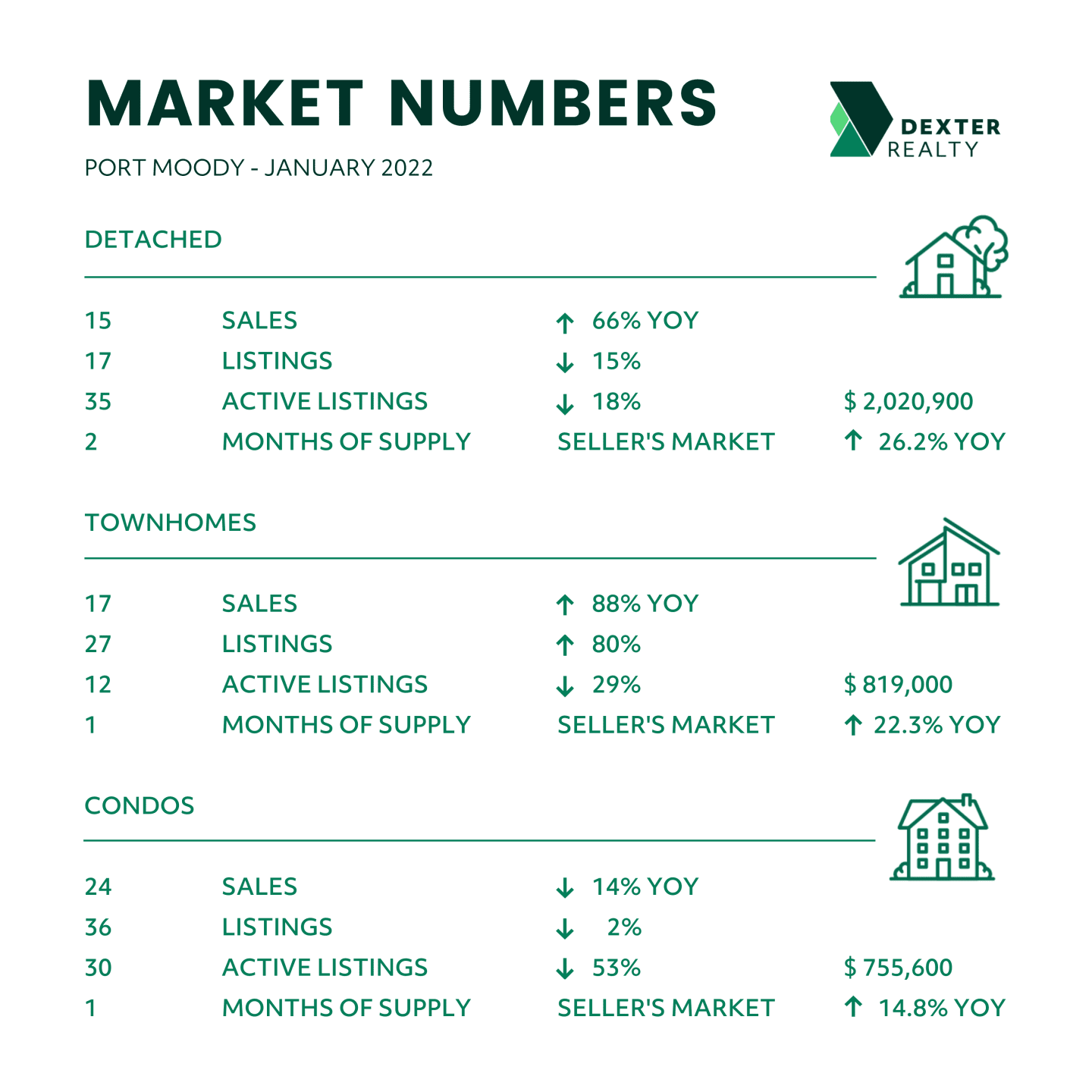

Port Moody: Total units sold in July were 45 – down from 57 (21%) in June 2022, and down 52% from July 2021. Active Listings were at 203 at month end compared to 161 at that time last year and 218 (down 7%) at the end of June; New Listings in July are down 31% compared to June 2022, but unchanged from a year earlier. Month’s supply of total residential listings is up to 5 month’s supply (balanced market conditions) and sales to listings ratio is 54% compared to 48% in June 2022. The composite benchmark price has slipped down about 2% from April to $1,197,300.

Port Coquitlam: Total units in July were 71 – down from 94 (24%) in June 2022 and 31% lower than in July 2021. Sales were also lower than in July 2020 and July 2019.

Active listings have held steady for two months at 212, representing a 3-month supply.

The sales ratio is at 52%. PoCo is having a quiet summer, but this remains a seller’s market with some bargain prices surfacing: the composite benchmark price has fallen 8.7% over the past three months to $946,100; and detached house prices are down 12% so far this year to $1,395,500.

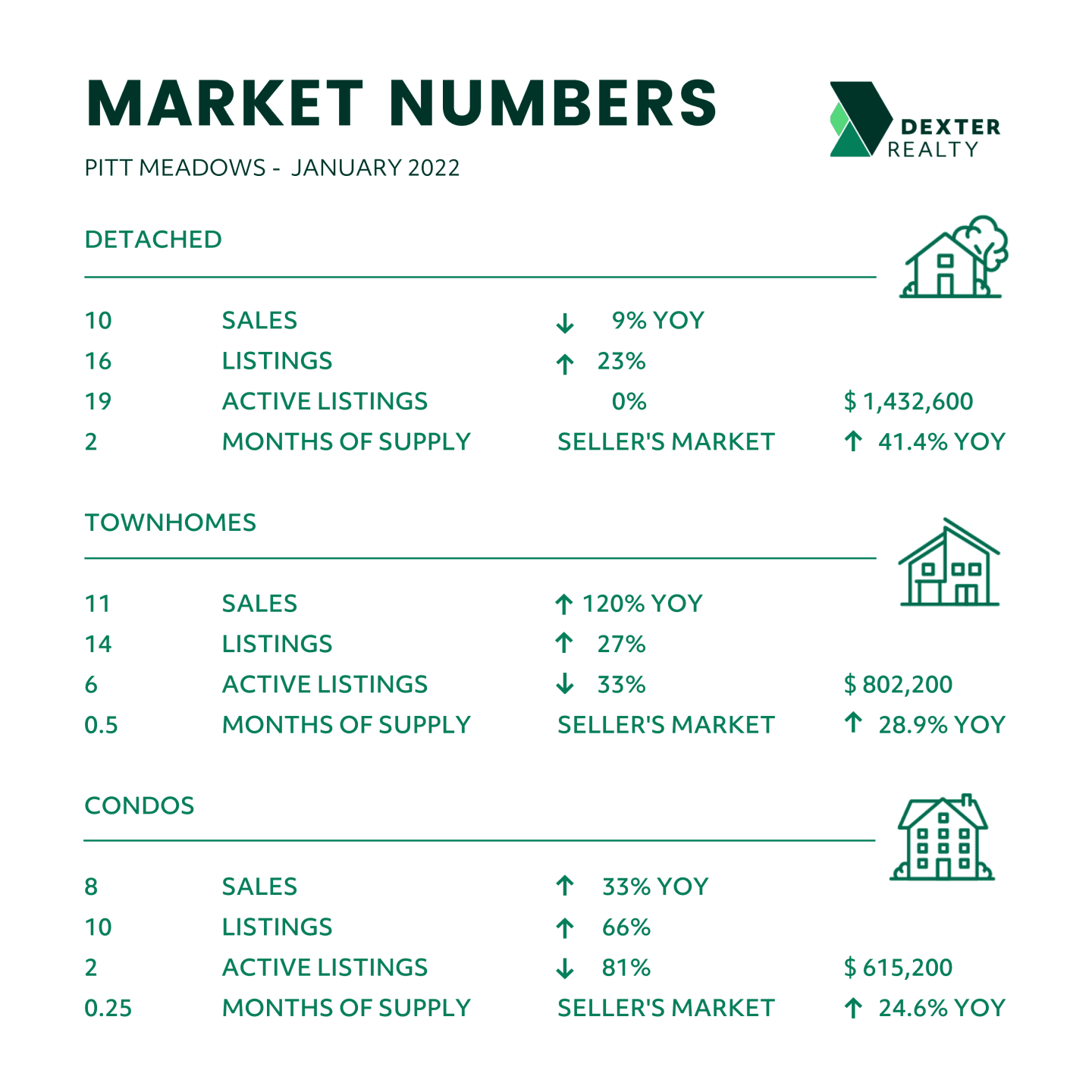

Pitt Meadows: Pitt Meadows had been one of the hot markets during the pandemic, but things change. Total housing sales this July, at 22, were down from both May and June of this year and 44% below July 2021. Active listings were 91 at the end of July, nearly double the 54 in July of last year, and new listings are up 31% from a year earlier. Detached-house benchmark prices have been falling since January and were down 9.3% from April to $1,335,900 in July. However, with a sales-to-listing ratio of 45% – compared to a sizzling 100% a year earlier – and about 4-month’s supply of homes on the market, this remains a seller’s advantage in a slow summer.

Maple Ridge: The benchmark detached house price in Maple Ridge apparently peaked in January and has been dropping ever since, down 8.7% since April to $1,343,800, which is also 3.4% lower than the start of this year. We may see more price corrections. Total sales in July were down 20% from June 2020 at 110 transactions, and 43% lower than in July 2021. Meanwhile, active listings increased to 638, up from 386 in July 2021. Maple Ridge is balanced and leaning towards a buyer’s market, with the sales-to-listing ratio dropping to 38% and a 6-month’s supply of homes for sale.

Ladner: Ladner is remaking its downtown and the waterfront village has perhaps too many summer distractions since homebuyers took a breather in July. Housing sales dropped 55% from month earlier and were down 67% from July 2021, one of the biggest declines in the Metro region. Total listings are rising and the sales-to-listing ratio is at 32%. This is a buyer’s market, with the composite home price falling steadily for six months and down 1.7% from a month earlier in July at $1,169,300, with an estimated 9-month’s supply of homes for sale.

Tsawwassen: With the popular Southlands development, townhouses have been one of the top housing sectors in Tsawwassen this year. We were seeing multiple bids in April and May of this year. Buyers will have noticed that prices have dropped since, with the typical townhouse selling in July for $989,600, the lowest price since January and down 4.6% since April. Detached house prices are also at the lowest level in 2022, down nearly 8% from three months ago, to $1,595,700. This is reflected in a sales decline, with July transactions of 40 homes down 30% from a month earlier and 52% below July 2021. We consider this a balanced market, with a 6-month’s supply and the sale success ratio at 50% in July, down from a ratio of 89% in the hot market of July 2021.

Surrey: B.C.’s second largest city has seen a dramatic shift in its housing market this year. Starts of new condos and townhouses have plunged 75% this year, dropping from 2,105 in the first six months of 2021 to just 509 units so far in 2022. Condo starts fell 77% year-to-year, based on CMHC data. July detached sales were down a startling 64% from July 2021 and were down 25.4% from June 2020 as the average price dropped 5.8% month-to-month to $1,662,928. Listings are down from 30% to 63% from a year earlier in the six Surrey neighbourhoods, but prices are holding steady in the townhouse ($876,500) and condo ($540,651) sectors. We are calling Surrey a buyer’s market that could get very active over the next few months.

Kevin Skipworth, Partner/Broker and Chief Economist at Dexter Realty