Highlights of Dexter’s November 2023 Report

New Westminster’s average price is the lowest in the region

Interest rates are coming down… soon.

2023 will have the lowest annual number of new listings since 2002

West Vancouver House Price Index down 3.7% month-over-month

BC NDP quickly pass a number of bills to boost supply and curb speculation

The numbers don’t paint a pretty picture. Month-over-month decline in sales, below the 10-year average, and low absorption rates mean fewer new listings are being bought. But there is an optimistic tone to the real estate market and one that will likely see the tilt towards more activity come after the Bank of Canada rate announcement on December 6th. The end of the rate increases has come and the tone to quicker and sooner rate decreases is upon us. The announcement by Canada’s Central Bank is more about tone than actual change in rates and judging by the commentary in markets and by economists, it's time to start the move downward.

December is always one of the slowest months for sales. The holiday season and the hangover after always impacts buyers and sellers. It’s more about decorating homes for the occasions than staging them for buyers. We’ve passed the high point in total listings, and the march to the end of the year will see less and less to choose from. But we’re still 13.4 percent higher than last year at this time. Whether January produces enough new listings to continue the price declines we’ve already seen in the last few months remains to be seen. But as we’ve said, buyers, your time is now.

November felt more like the 12 Housing Announcements for Christmas with provincial and federal governments putting forward policy after policy on how to create affordability and build more homes. From programs to help buyers save, to density in neighbourhoods and around transit to eliminating short-term rentals in many regions across British Columbia. Nary a stone was left unturned when it came to putting policy forward in November. Will it work? That’s the big question. Will it produce 130,000 homes over the next 10 years in British Columbia and reduce prices by 14% as claimed by the BC NDP? Without modelling, it’s just a wish and one that the NDP has made for Christmas with the numerous bills passed in the legislature at the end of November.

Below 2,000 we continue to go as there were 1,702 properties of all types sold in Greater Vancouver in November after seeing 1,996 sales in October. A similar trend to last year through the fall, although this year’s numbers have been higher. There were 1,625 sales in Greater Vancouver in November 2022 – so it is not all bad in the market especially when we look at 2018 when there were 1,633 sales in November. Total sales for 2023 in Greater Vancouver will likely finish just over 26,000 – down from the 29,227 in 2022. Although this would still be higher than the total sales for the years of 2018 and 2019 at 25,051 and 25,679 respectively. But alas, sales in November were 35% below the 10-year average, compared to 31% below the 10-year average in October.

There is optimism in the real estate market. Perhaps the lack of rate increases by the Bank of Canada through the fall gave some buyers and sellers reason to break free of the stalemate. There’s a noticeable uptick in activity for some listings and it’s resulting in sales for some longer-standing listings.

With current sales, we are in a balanced market with 6 months supply of homes overall in Greater Vancouver while some areas are experiencing less inventory and positioned more in a seller’s market based on total inventory. North Vancouver and Port Moody are sitting with 3 3-month supply, while Burnaby North and South, New Westminster and Port Coquitlam were left with 4 4-month supply. Coquitlam has seen quick growth in inventory in the last 2 months, going from 599 active listings in August to 778 at the end of October. This growth is mainly in the condo and townhouse sectors but still sits with 4 4-month supply.

There were 3,440 new listings in November after 4,752 new listings in October, compared with 5,557 new listings in September, and slightly higher than the number of new listings in November last year at 3,141. By the end of 2023 though, there will likely be 51,500 total new listings for the year which would be the lowest annual new listing count going back to 2002.

The number of new listings in November had declined to 3% above the 10-year average, compared with October with the count being 5% above the 10-year average and September with 6% above the 10-year average. We are seeing more new listings in comparison to sales levels which is helping keep active listing counts higher than the last two years, meaning more opportunity for buyers and with a slower pace of sales, the opportunity to negotiate and have time for due diligence.

There were 10,931 active listings at month end in Greater Vancouver compared with 11,599 active listings at the end of November and 11,382 active listings at the end of September. With absorption rates much lower than is typical for November, listings are staying on the market longer and the traditional decline in active listings we are seeing in the later part of the year has been much slower. While all areas saw a decline in active listings overall, in some areas there was an increase in condo inventory month-over-month. The detached market overall remains in buyer’s market territory with 8 months supply of inventory but during the month of November the absorption rate was the highest at 52% compared to townhomes and condos, in part to lesser growth in new listings. Townhomes and condos sit just above 5 months supply of listings, bordering on a balanced market after being in seller’s market territory for some time.

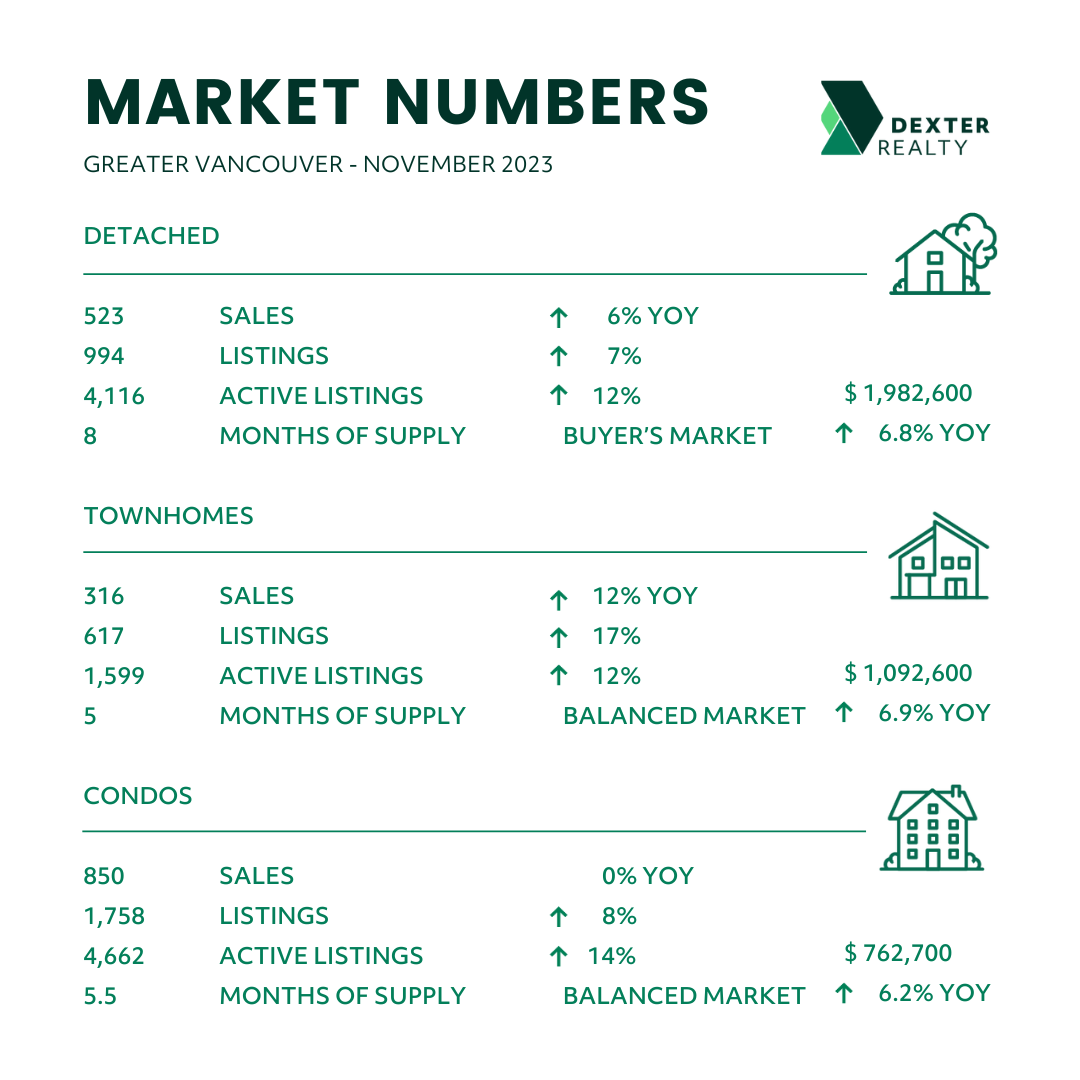

Here’s a summary of the numbers:

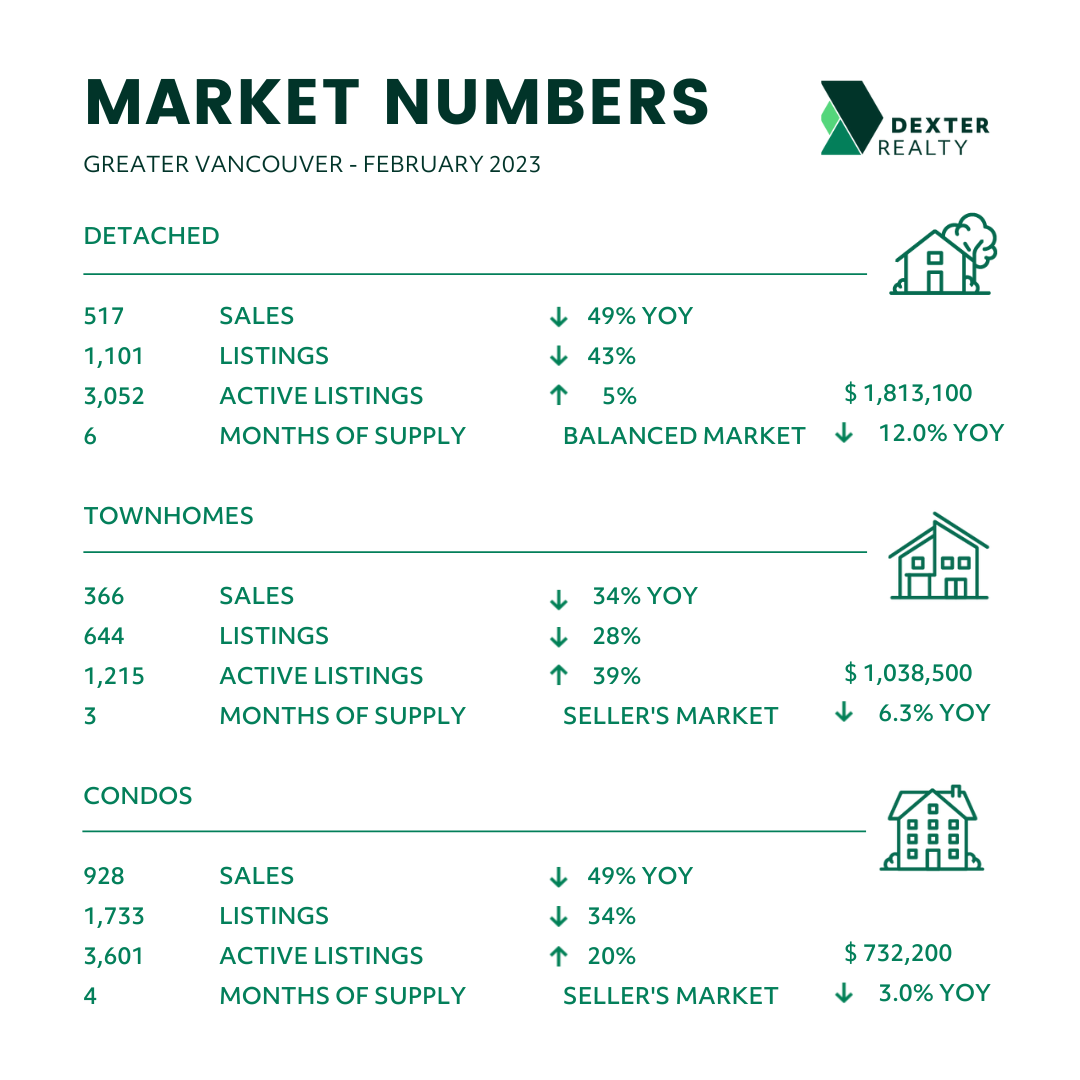

Greater Vancouver: Month-over-month, the house price index is down 1% and only up 4.9% year-over-year. Total Units Sold in November were 1,702, down from 1,996 (15%) in October 2023, down from 1,926 (12%) in September 2023, up from 1,625 (5%) in November 2022, down from 3,492 (51%) in November 2021, down from 3,131 (46%) in November 2020, down from 2,546 (33%) in November 2019; Active Listings were at 10,931 at month end compared to 9,633 at that time last year and 11,599 at the end of October; New Listings in November were down 28% compared to October 2023, down 38% compared to September 2023, up 10% compared to November 2022, down 15% compared to November 2021, down 17% compared to November 2020 and up 12% compared to November 2019. Month’s supply of total residential listings is steady at 6 month’s supply (balanced market conditions – detached homes at 8 months supply, a buyer’s market) and sales to listings ratio of 49% compared to 42% in October 2023, 52% in November 2022 and 87% in November 2021.

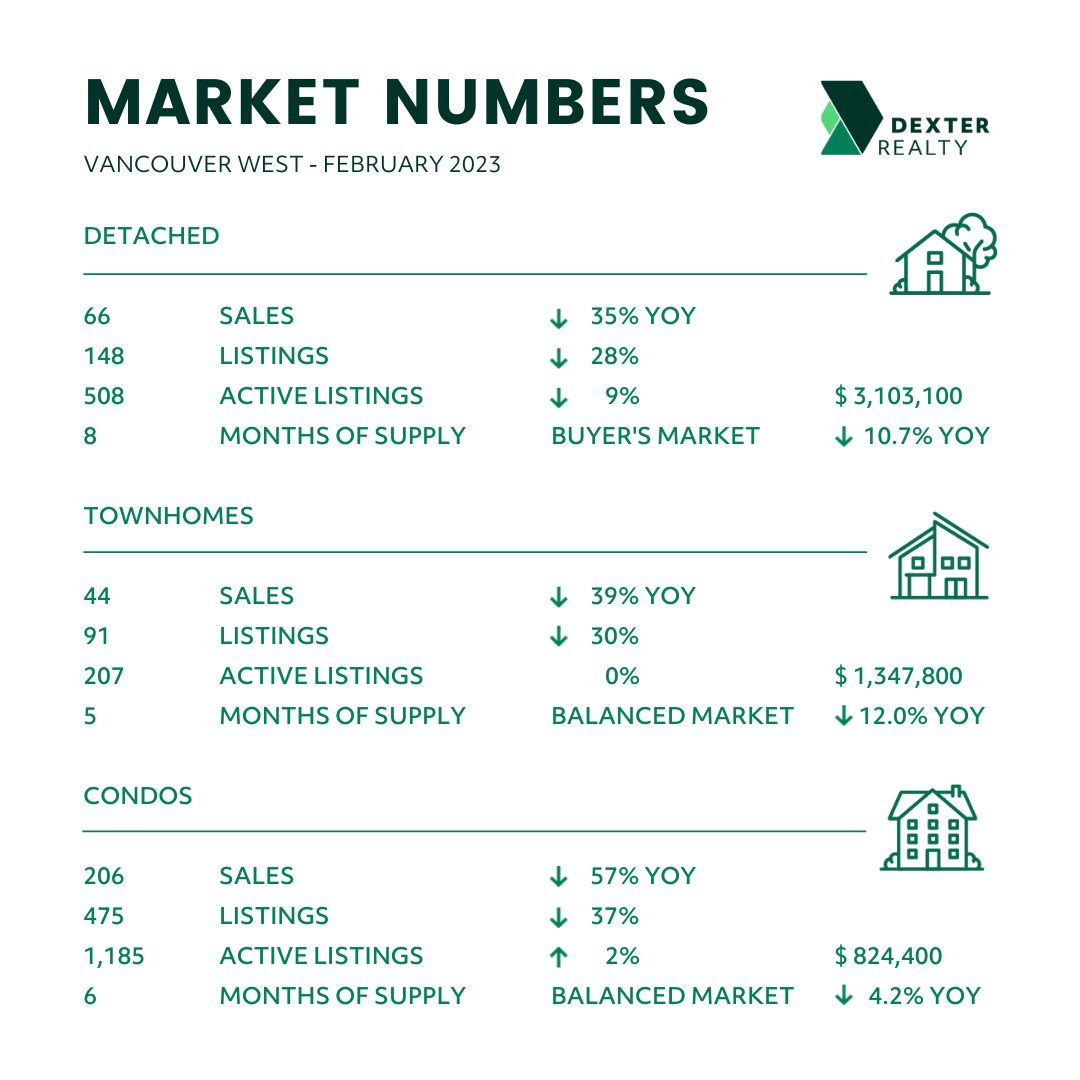

Vancouver Westside: The detached home price index was up 0.9% last month, and up 9.8% over last year – the highest in the region. Total Units Sold in November were 315, down from 352 (10%) in October 2023, down from 338 (7%) in September 2023, up from 306 (%3) in November 2022, down from 647 (51%) in November 2021, down from 470 (33%) in November 2020, down from 406 (22%) in November 2019. Detached and townhouses sales were up year-over-year while condo sales were flat compared to last year. Active Listings were at 2,432 at month end compared to 2,300 at that time last year and 2,629 at the end of October – detached active listings down year-over-year – an anomaly in the market. New Listings in November were down 32% compared to October 2023, down 41% compared to September 2023, down 10% compared to November 2022, down 22% compared to November 2021, down 16% compared to November 2020 and up 19% compared to November 2019. Month’s supply of total residential listings is up to 8 month’s supply (buyer’s market conditions) and sales to listings ratio of 47% compared to 35% in October 2023, 41% in November 2022 and 75% in November 2021.

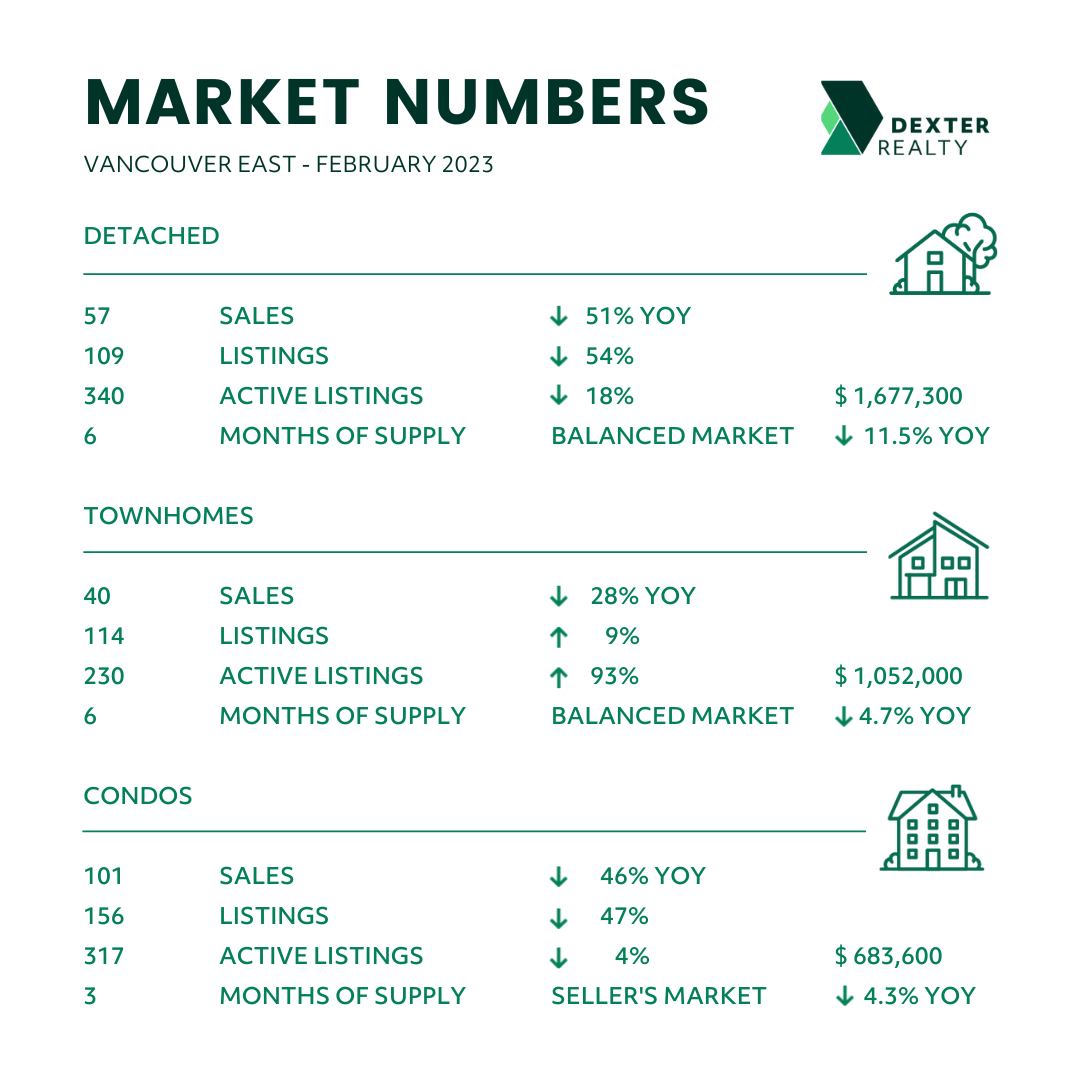

Vancouver East Side: The house price index was up 8.9% over last year – a trend for Vancouver overall that will continue as the supply of detached homes declines due to densification. Total Units Sold in November were 175, down from 231 (24%) in October 2023, down from 192 (9%) in September 2023, up from 167 (5%) in November 2022, down from 385 (54%) in November 2021, down from 364 (52%) in November 2020, down from 310 (43%) in November 2019; Active Listings were at 1,238 at month end compared to 1,045 at that time last year and 1,265 at the end of October (townhouse active listing counts were up compared to October); New Listings in November were down 28% compared to October 2023, down 35% compared to September 2023, up 23% compared to November 2022 (townhouses were up 46%), down 19% compared to November 2021, down 14% compared to November 2020 and up 20% compared to November 2019. Month’s supply of total residential listings is up to 7 month’s supply (balanced market conditions) and sales to listings ratio of 43% compared to 41% in October 2023, 50% in November 2022 and 76% in November 2021.

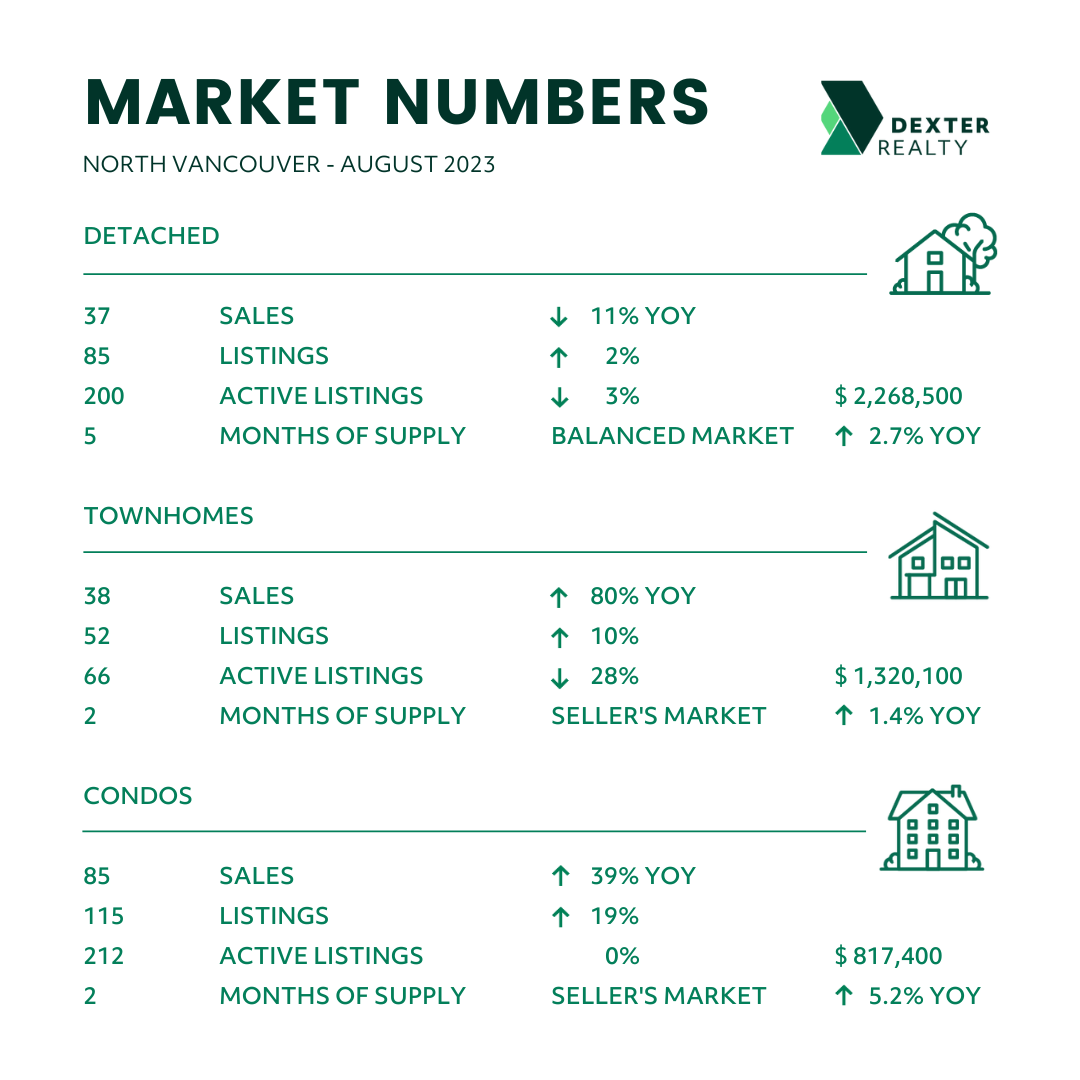

North Vancouver: One of the few seller’s markets for inventory in Metro Vancouver. Total Units Sold in November were 157, down from 194 (19%) in October 2023, down from 169 (7%) in September 2023, up from 149 (5%) in November 2022, down from 247 (36%) in November 2021, down from 264 (40%) in November 2020, down from 217 (28%) in November 2019; Active Listings were at 560 at month end compared to 529 at that time last year and 621 at the end of October; New Listings in November were down 28% compared to October 2023, down 44% compared to September 2023, up 3% compared to November 2022, down 7% compared to November 2021, down 20% compared to November 2020 and up 17% compared to November 2019. Month’s supply of total residential listings is up to 4 month’s supply (seller’s market conditions) and sales to listings ratio of 59% compared to 52% in October 2023, 57% in November 2022 and 87% in November 2021.

West Vancouver: West Vancouver saw the house price index drop by 3.7% last month, strangely driven by a 3.8% decline in the condo house price index. Detached sales in November were 33 compared to 16 in November 2022, with the overall average price jumping to the highest figure since May 2022. Total Units Sold in November were 48, down from 53 (9%) in October 2023, down from 53 (9%) in September 2023, up from 28 (71%) in November 2022, down from 81 (41%) in November 2021, down from 90 (47%) in November 2020, down from 66 (27%) in November 2019; Active Listings were at 593 at month end compared to 561 at that time last year and 609 at the end of October; New Listings in November were down 16% compared to October 2023, down 44% compared to September 2023, up 25% compared to November 2022, up 22% compared to November 2021, down 25% compared to November 2020 and up 21% compared to November 2019. Month’s supply of total residential listings is up to 12 month’s supply (buyer’s market conditions) and sales to listings ratio of 34% compared to 32% in October 2023, 25% in November 2022 and 70% in November 2021.

Richmond: Strength in the detached market saw the house price index rise 0.3% last month. Total Units Sold in November were 179, down from 217 (17%) in October 2023, down from 256 (30%) in September 2023, down from 210 (15%) in November 2022 (detached sales were up year-over-year), down from 481 (63%) in November 2021, down from 335 (47%) in November 2020, down from 273 (34%) in November 2019; Active Listings were at 1,258 at month end compared to 1,108 at that time last year and 1,268 at the end of October (condo active listings were up month-over-month); New Listings in November were down 16% compared to October 2023, down 32% compared to September 2023, up 36% compared to November 2022, down 21% compared to November 2021, down 23% compared to November 2020 and up 5% compared to November 2019. Month’s supply of total residential listings is up to 7 month’s supply (balanced market conditions) and sales to listings ratio of 44% compared to 45% in October 2023, 70% in November 2022 and 94% in November 2021.

Burnaby East: Total Units Sold in November were 13, down from 21 (38%) in October 2023, down from 18 (28%) in September 2023, down from 14 (7%) in November 2022, down from 33 (61%) in November 2021, down from 37 (65%) in November 2020, down from 33 (61%) in November 2019; Active Listings were at 93 at month end compared to 88 at that time last year and 105 at the end of October (condo active listing count up month-over-month and year-over-year); New Listings in November were down 37% compared to October 2023, down 39% compared to September 2023, down 19% compared to November 2022, down 23% compared to November 2021, down 21% compared to November 2020 and down 19% compared to November 2019. Month’s supply of total residential listings is up to 7 month’s supply (balanced market conditions) and sales to listings ratio of 43% (detached at 86%) compared to 44% in October 2023, 38% in November 2022 and 85% in November 2021. The house price index was down 2.2% last month only up 4.6% since last year.

Burnaby North: Total Units Sold in November were 119, down from 137 (13%) in October 2023, up from 113 (5%) in September 2023, up from 92 (29%) in November 2022, down from 185 (36%) in November 2021, down from 156 (24%) in November 2020, down from 137 (13%) in November 2019; Active Listings were at 549 at month end compared to 416 at that time last year and 598 at the end of October; New Listings in November were down 36% compared to October 2023, down 39% compared to September 2023, up 16% compared to November 2022, down 15% compared to November 2021, down 24% compared to November 2020 and up 42% compared to November 2019. Month’s supply of total residential listings is up to 5 month’s supply (balanced market conditions) and sales to listings ratio of 64% (90% for townhomes) compared to 47% in October 2023, 57% in November 2022 and 84% in November 2021. The house price index was down 1.8% year-over-year.

Burnaby South: Total Units Sold in November were 83, down from 120 (31%) in October 2023, down from 126 (34%) in September 2023, down from 118 (30%) in November 2022, down from 225 (63%) in November 2021, down from 159 (48%) in November 2020, down from 167 (50%) in November 2019; Active Listings were at 487 at month end compared to 425 at that time last year and 515 at the end of October; New Listings in November were down 27% compared to October 2023, down 40% compared to September 2023, down 5% compared to November 2022, down 26% compared to November 2021, down 19% compared to November 2020 and down 5% compared to November 2019. Month’s supply of total residential listings is up to 6 month’s supply (balanced market conditions) and sales to listings ratio of 50% compared to 53% in October 2023, 68% in November 2022 and 100% in November 2021. The house price index was down 1.4% year-over-year.

New Westminster: With an average price of $775,593, New Westminster continues to offer the best value in the region. And the house price index at $828,200 is only $7,400 above the Sunshine Coast. Total Units Sold in November were 65, down from 81 (20%) in October 2023, down from 72 (10%) in September 2023, the same as 65 in November 2022, down from 177 (63%) in November 2021, down from 137 (53%) in November 2020, down from 123 (47%) in November 2019; Active Listings were at 302 at month end compared to 292 at that time last year and 305 at the end of October; New Listings in November were down 14% compared to October 2023, down 24% compared to September 2023, up 2% compared to November 2022, down 27% compared to November 2021, down 22% compared to November 2020 and up 35% compared to November 2019. Month’s supply of total residential listings is up to 5 month’s supply (balanced market conditions) and sales to listings ratio of 50% compared to 53% in October 2023, 51% in November 2022 and 99% in November 2021.

Coquitlam: The house price index is only up 2.7% year-over-year, more inventory is helping keep prices in check. Total Units Sold in November were 159, down from 167 (5%) in October 2023, down from 170 (%) 6in September 2023, up from 134 (19%) in November 2022, down from 289 (45%) in November 2021, down from 260 (39%) in November 2020, down from 210 (24%) in November 2019; Active Listings were at 721 at month end compared to 582 at that time last year and 778 at the end of October; New Listings in November were down 29% compared to October 2023, down 35% compared to September 2023, up 17% compared to November 2022, down 10% compared to November 2021, down 23% compared to November 2020 and up 34% compared to November 2019. Month’s supply of total residential listings is steady at 5 month’s supply (detached in a buyer’s market and townhomes and condos a seller’s market) and sales to listings ratio of 55% compared to 41% in October 2023, 54% in November 2022 and 89% in November 2021.

Port Moody: This is an inventory starved market, hopefully proposed development along St.Johns Steet will help. Even with low inventory, the house price index is down 1.2% from last month. Total Units Sold in November were 40, down from 51 (12%) in October 2023, down from 44 (9%) in September 2023, up from 33 (21%) in November 2022 – condo sales were up 72% year-over-year, down from 61 (34%) in November 2021, down from 67 (40%) in November 2020, down from 43 (7%) in November 2019; Active Listings were at 166 at month end compared to 194 at that time last year and 170 at the end of October; New Listings in November were up 1% compared to October 2023, down 17% compared to September 2023, up 2% compared to November 2022, up 18% compared to November 2021, up 1% compared to November 2020 and up 79% compared to November 2019. Month’s supply of total residential listings is up to 4 month’s supply (seller’s market conditions) and sales to listings ratio of 47% compared to 60% in October 2023, 38% in November 2022 and 84% in November 2021.

Port Coquitlam: Another one of the few municipalities with seller’s market conditions. Total Units Sold in November were 55, up from 54 (2%) in October 2023, down from 65 (15%) in September 2023, up from 39 (13%) in November 2022 – townhouse sales were up 142% year-over-year, down from 127 (57%) in November 2021, down from 102 (56%) in November 2020, down from 90 (39%) in November 2019; Active Listings were at 183 at month end compared to 183 at that time last year and 201 at the end of October; New Listings in November were down 21% compared to October 2023, down 35% compared to September 2023, down 1% compared to November 2022, down 21% compared to November 2021, down 24% compared to November 2020 and down 27% compared to November 2019. Month’s supply of total residential listings is down to 3 month’s supply (seller’s market conditions) and sales to listings ratio of 61% (113% for townhouses) compared to 47% in October 2023, 43% in November 2022 and 111% in November 2021. The house price index is down 0.7% from last month but up 6.2% from last year.

Pitt Meadows: Total Units Sold in November were 21, the same as 21 in October 2023, down from 24 (12%) in September 2023, down from 22 (4%) in November 2022, down from 32 (34%) in November 2021, down from 46 (54%) in November 2020, down from 24 (12%) in November 2019; Active Listings were at 83 at month end compared to 82 at that time last year and 91 at the end of October; New Listings in November were down 17% compared to October 2023, down 28% compared to September 2023, up 39% compared to November 2022, down 11% compared to November 2021, up 3% compared to November 2020 and up 105% compared to November 2019. Month’s supply of total residential listings is down to 4 month’s supply (seller’s market conditions) and sales to listings ratio of 53% compared to 44% in October 2023, 78% in November 2022 and 72% in November 2021. The house price index was down 0.8% last month but up 5.7% since last year.

Maple Ridge: Total Units Sold in November were 103, down from 110 (6%) in October 2023, down from 108 (5%) in September 2023, up from 94 (10%) in November 2022, down from 198 (48%) in November 2021, down from 176 (41%) in November 2020, down from 169 (39%) in November 2019; Active Listings were at 718 at month end compared to 543 at that time last year and 774 at the end of October; New Listings in November were down 39% compared to October 2023, down 44% compared to September 2023, up 4% compared to November 2022, down 8% compared to November 2021, down 2% compared to November 2020 and down 6% compared to November 2019. Month’s supply of total residential listings is steady at 7 month’s supply (balanced market conditions) and sales to listings ratio of 51% compared to 33% in October 2023, 49% in November 2022 and 90% in November 2021. The house price index was down 1.7% last month but up 4.3% since last year.

Ladner: Total Units Sold in November were 21, down from 24 (12%) in October 2023, down from 26 (19%) in September 2023, up from 16 (31%) in November 2022, down from 41 (49%) in November 2021, down from 47 (55%) in November 2020, down from 42 (50%) in November 2019; Active Listings were at 104 at month end compared to 83 at that time last year and 119 at the end of October; New Listings in November were down 41% compared to October 2023, down 60% compared to September 2023, up 13% compared to November 2022, down 35% compared to November 2021, down 32% compared to November 2020 and down 49% compared to November 2019. Month’s supply of total residential listings is steady at 5 month’s supply (balanced market conditions) and sales to listings ratio of 81% (100% for townhomes and condos) compared to 55% in October 2023, 70% in November 2022 and 103% in November 2021. The house price index was down 2.0% last month, but up 6.4% since last year.

Tsawwassen: Total Units Sold in November were 20, down from 27 (26%) in October 2023, down from 42 (52%) in September 2023, down from 31 (35%) in November 2022, down from 52 (61%) in November 2021, down from 55 (64%) in November 2020, down from 36 (44%) in November 2019; Active Listings were at 180 at month end compared to 150 at that time last year and 188 at the end of October; New Listings in November were down 40% compared to October 2023, down 39% compared to September 2023, up 50% compared to November 2022, down 8% compared to November 2021, down 42% compared to November 2020 and up 2% compared to November 2019. Month’s supply of total residential listings is up to 9 month’s supply (buyer’s market conditions) and sales to listings ratio of 44% compared to 36% in October 2023, 103% in November 2022 and 106% in November 2021. Tsawwassen showed a 0.9% increase in the house price index last month, up 6.3% since last year.

Fraser Valley: Sales in November were down 8.1% from October but up 6.2% from November 2022. New listings were down 19.9% from October but up 19.2% from November 2022. While the average price was unchanged month-over-month, it is up 10.4% from November 2022. Active listings were down 5% from last month but up 17% from November 2022. “As we head into the holiday season, buyers and sellers are busy with other priorities and will most likely continue to wait on the sidelines,” said Narinder Bains, Chair of the Fraser Valley Real Estate Board. “We anticipate this holding pattern, defined by slow sales and declining new listings, will continue through the winter months until we see some downward movement in interest rates.”

Kevin Skipworth, Partner/Broker and Chief Economist at Dexter Realty