Highlights of Dexter’s February 2026 report

February sales jump up from January

Absorption improving across multiple areas

Inventory continues to expand in a controlled and constructive way

Vancouver market showed a strong February rebound

February Market Overview: Momentum Building with Room to Improve

February delivered exactly what a transitional market needs: momentum. Slow but sure. After a tepid and more cautious start to the year, activity across Greater Vancouver accelerated in February, supported by improving buyer engagement, inventory growth, and a shift toward more balanced conditions in some of the submarkets.

While sales remain below the elevated levels seen during the post-pandemic surge years, the direction of the market is what matters most and February showed measurable improvement in nearly every key indicator. We just need more of that improvement going forward.

Total residential sales in Greater Vancouver reached 1,648 units, rising sharply by 49% from January and surpassing December levels as seasonal demand returned as expected. This type of early-year acceleration typically signals that underlying demand has been building quietly and is now beginning to re-engage as buyers adapt to current pricing and today’s interest rate environment. There is still significant pent-up demand though, which will continue to impact the market when those buyers start to engage at a greater level. With sales for the month of February at the lowest since 2019, there is plenty of that pent-up demand. As interest rate renewals impact homeowners, from the extreme lows of 2021 to current rates, there will be more motivation for some to make a move.

At the same time, inventory continues to expand in a controlled and constructive way. Active listings rose to 13,545 units, up 6% year-over-year and 7% month-over-month. This increase is not a sign of weakness; it represents improving choice and continued opportunities for buyers which is healthier for the market. The rapid supply shortages that defined previous cycles are giving way to a more sustainable balance between buyers and sellers.

New listings totaled 4,826 units in February, down from January partly due to the shorter month but perhaps also signaling a sign of seller exhaustion. This confirms a pattern that has been building since late 2025: sellers are not overwhelming the market.

Perhaps the most notable shift is the improvement in absorption. The sales-to-listings ratio climbed to 34%, up from 21% in January. Months of supply tightened from 11 months to 8 months, still technically within buyer-leaning conditions, but moving decisively toward balance. And in some areas balance was achieved. The townhome segment more so.

Markets rarely turn overnight. They stabilize first. February shows that stabilization phase is well underway.

A Market Transitioning Toward Balance

One of the defining characteristics of the current cycle is structure. Unlike the volatility seen between 2020 and 2022, the market is now progressing through a far more disciplined transition. Caution best describes this market right now. Demand is not surging indiscriminately; it is returning selectively.

Buyers are active where pricing aligns with value. Sellers that are motivated are adjusting expectations accordingly. This dynamic is creating steady absorption rather than speculative spikes, which is exactly what long-term market health requires.

Across most submarkets, months of supply declined materially compared to January. This indicates that while inventory remains elevated relative to past years, in some areas, demand is beginning to catch up.

Balanced conditions are expanding geographically, particularly across the Tri-Cities and some urban markets.

Greater Vancouver sales in February were 29% below the 10-year average after January was 31% below the 10-year average. While February’s numbers appeared to be low, overall, it is an improvement from January in looking longer term. Geopolitical and economic conditions continue to weigh on the market, with local politics not helping the matter either.

The number of new listings in February were 7% above the 10-year average, after January was 19% above the 10-year average and December was 11%. Buyers take note that opportunities of abundance could be changing as sellers pull away from a buyer’s market.

Vancouver Market Strength Returning

The city markets showed strong February rebounds, particularly across both sides of the city.

Vancouver Westside

Sales increased 57% month-over-month to 298 transactions, while the sales-to-listings ratio improved to 34%. Months of supply tightened from 12 months to 8 months, a meaningful improvement.

Inventory remains elevated, but demand is beginning to absorb it at a more sustainable pace with sales in February closer aligned to February of last year.

Vancouver East Side

The East Side delivered one of the strongest performances in the region. Sales jumped 73% from January and 8% above February last February. Months of supply fell dramatically from 10 months to 6 months, moving firmly into balanced territory. The sales-to-listings ratio rose to 42%, reflecting strong absorption in family-oriented price ranges. This market continues to benefit from better affordability compared to the Westside

North Shore: Tale of Two Markets

North Vancouver posted a 47% month-over-month increase in sales, while months of supply tightened to 6 months giving that area balanced market conditions. Inventory has increased year-over-year, but demand is clearly improving alongside it. The combination of lifestyle demand and limited long-term supply continues to support pricing stability.

West Vancouver remains a slower-moving luxury market, though even here improvement is visible. Sales increased month-over-month, and months of supply declined slightly to 18 months.

Luxury markets typically lag broader recoveries.

Beyond Vancouver

Richmond showed modest month-over-month sales growth but continues to be a strong buyer’s market. Inventory remains elevated at 12 months of supply.

The Burnaby markets collectively showed steady improvement.

Burnaby East saw sales more than double month-over-month, while months of supply dropped sharply from 16 months to 9 months. Burnaby North and South saw more moderate gains and sales-to-listings ratios up significantly from last month.

Burnaby continues to benefit from its central location and strong condo and townhome demand tied to transit-oriented development.

Sales in New Westminster surged 58% month-over-month while months of supply fell to 7 months. This market has quietly become one of the most balanced in the region, supported by strong first-time buyer demand and relative affordability.

Coquitlam posted one of the largest increases in activity, with sales rising 83% from January. Months of supply fell from 12 months to 7 months—another strong indicator of market stabilization.

Port Moody continued its sluggish start to the year, with newer product on the way.

Port Coquitlam stands out as one of the strongest-performing markets this month, with a 46% sales-to-listings ratio—solidly within balanced territory. Townhouse sales surged from 6 to 22 in February with more sales than new listings. Mayor Brad West said that provincial policies on density have restricted townhouse development – these numbers seem to support that. Buyers should cross over the bridge into Pitt Meadows with its 13 months supply of townhomes albeit still only 40 active listings.

Ladner experienced one of the most dramatic shifts in the region. Months of supply dropped from 29 months to just 6 months, a rapid normalization driven by a sharp increase in sales activity. The sales-to-listings ratio jumped to 43%, demonstrating how quickly smaller markets can rebalance once demand returns. While Tsawwassen also showed improving structure, with inventory stabilizing and sales rising month-over-month.

Fraser Valley Tells a Similar Story as Greater Vancouver

The Fraser Valley market acted much like Greater Vancouver in February with stronger month-over-month sales and weaker month-over-month new listings, but still down from last year in both categories. With 843 sales in February, this was up 36% from January and down 8% from February 2025. February sales in the Fraser Valley were the lowest for the month of February since 2000. Surrey continues to struggle in that market, with outer areas showing more improvement in sales activity, particularly in the townhouse segment.

With the increase in sales last month, months of supply in the Fraser Valley decreased from 12 months in January to 10 months in February and compared to 9 months in February 2025. This is a market that continues to struggle.

The Bigger Picture: Inventory Is a Feature, Not a Problem

One of the most important narratives shaping the 2026 market is the role of inventory.

For several years, the dominant market constraint was lack of supply. Today, that constraint has eased, but not in a way that weakens the market. Instead, it is creating opportunity. The drop in months of supply from 11 to 8 across the region confirms that demand is already adjusting to this new environment. February’s performance matters because it sets the tone for the spring market.

Historically, when February shows strong month-over-month gains, as seen with the 49% increase in sales, March and April often build on that momentum. Time for buyers to spring into action!

Here’s a summary of the numbers:

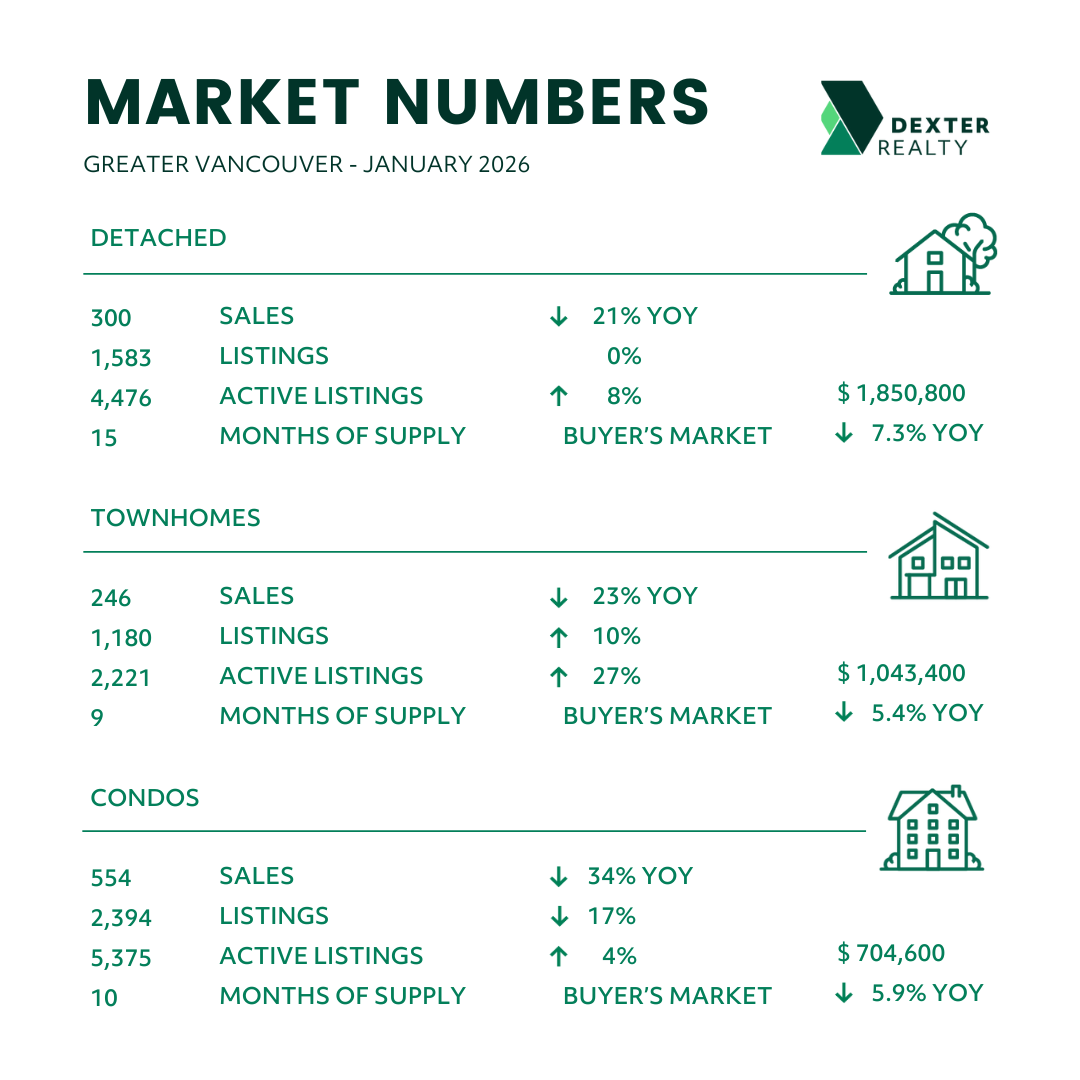

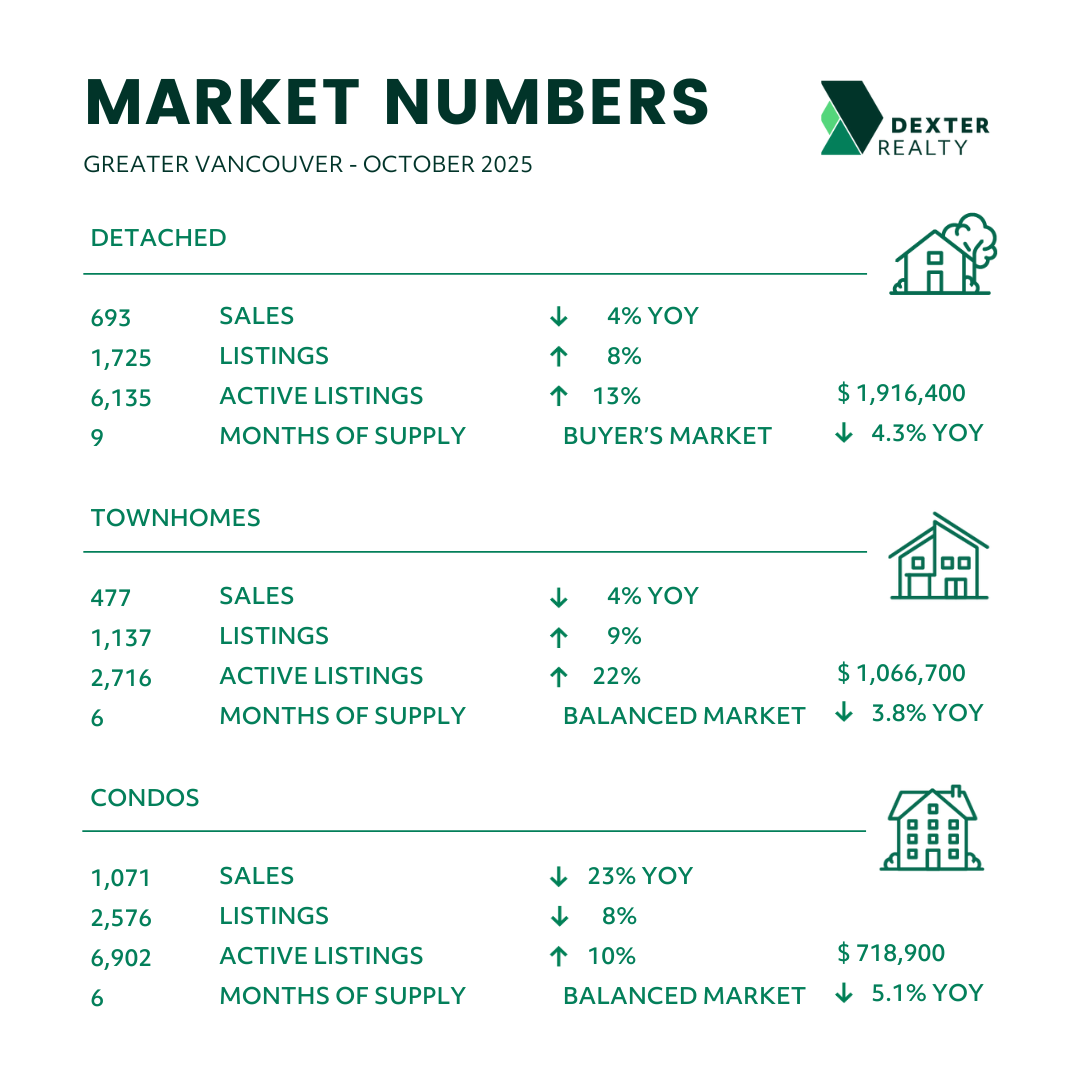

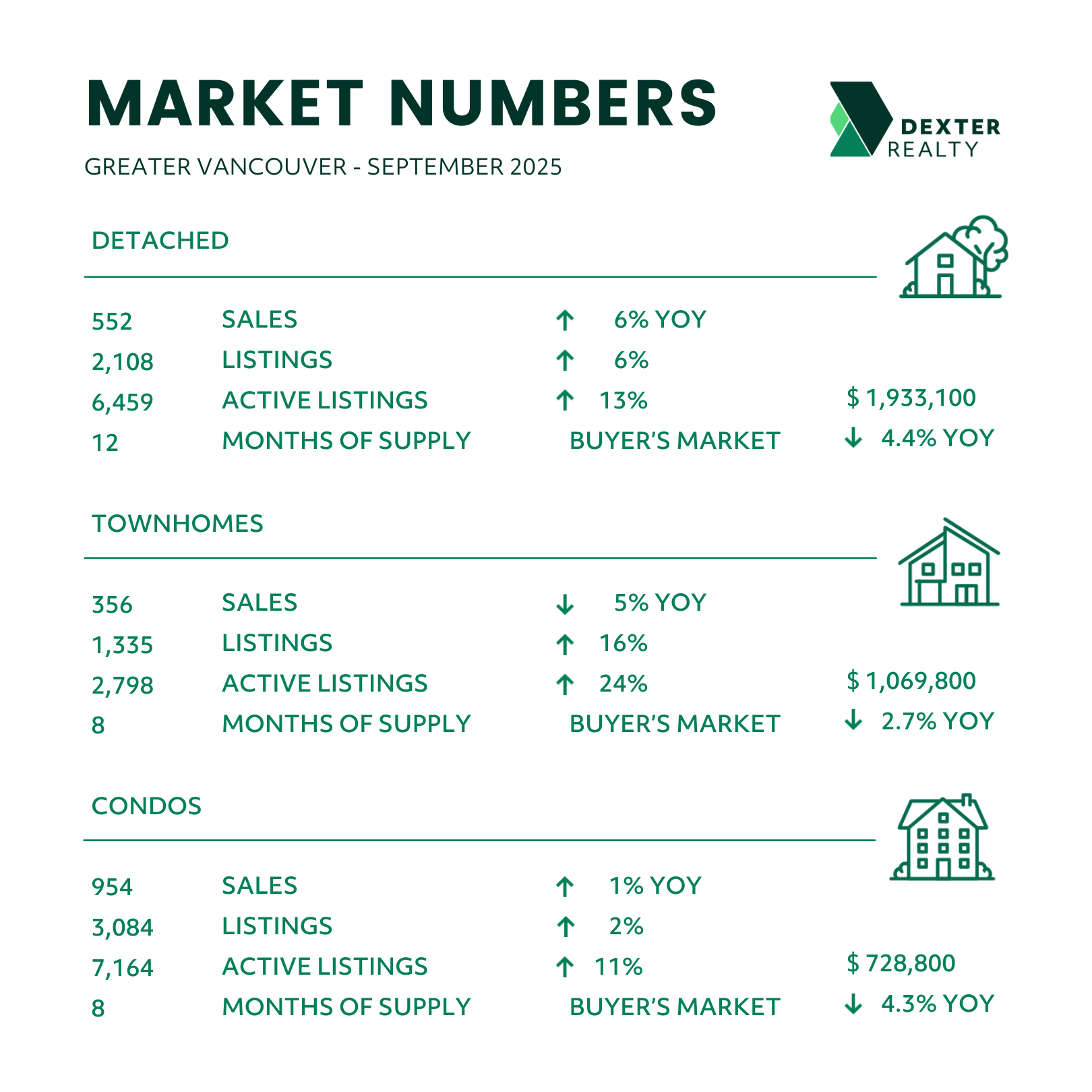

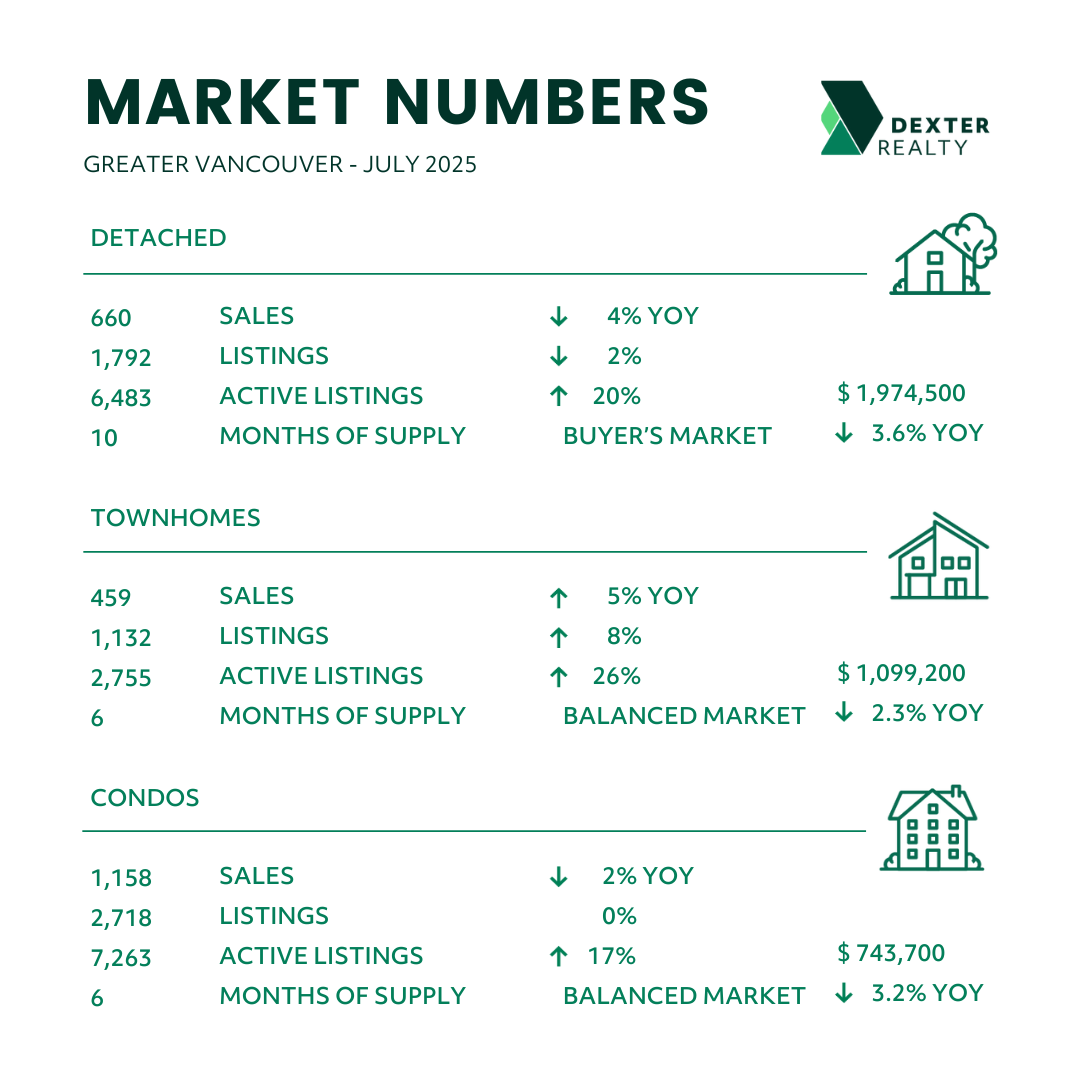

Greater Vancouver: Total Units Sold in February were 1,648, up from 1,107 (49%) in January, up from 1,537 (7%) in December, down from 1,846 (11%) in November, down from 1,827 (10%) in February 2025, down from 2,070 (20%) in February 2024, and down from 1,824 (10%) in February 2023; Active Listings were at 13,545 at month end compared to 12,744 at that time last year (up 6%) and 12,628 at the end of January (up 7%); the 4,826 New Listings in February were down 8% compared to January, up 153% compared to December, up 29% compared to November, down 7% compared to February 2025, up 4% compared to February 2024 and up 36% compared to February 2023. Month’s supply of total residential listings is down to 8 months from 11 (buyer’s market conditions) and sales to listings ratio of 34% compared to 21% in January 2026, 35% in February 2025, 45% in February 2024 and 51% in February 2023.

Vancouver Westside: Total Units Sold in February were 298, up from 190 (57%) in January, up from 287 (4%) in December, down from 363 (18%) in November, down from 307 (3%) in February 2025, down from 374 (20%) in February 2024, and down from 316 (6%) in February 2023; Active Listings were at 2,470 at month end compared to 2,780 at that time last year (up 11%) and 2,301 at the end of January (up 7%); the 870 New Listings in February were down 5% compared to January, up 174% compared to December, up 23% compared to November, down 19% compared to February 2025, down 7% compared to February 2024 and up 22% compared to February 2023. Month’s supply of total residential listings is down to 8 months from 12 (buyer’s market conditions) and sales to listings ratio of 34% compared to 21% in January 2026, 29% in February 2025, 40% in February 2024 and 44% in February 2023.

Vancouver East Side: Total Units Sold in February were 220, up from 127 (73%) in January, up from 158 (39%) in December, up from 210 (5%) in November, up from 204 (8%) in February 2025, down from 249 (12%) in February 2024, and up from 198 (11%) in February 2023; Active Listings were at 1,391 at month end compared to 1,313 at that time last year (up 6%) and 1,329 at the end of January (up 5%); the 524 New Listings in February were down 20% compared to January, up 139% compared to December, up 24% compared to November, down 8% compared to February 2025, down 4% compared to February 2024 and up 37% compared to February 2023. Month’s supply of total residential listings is down to 6 months from 10 (balanced market conditions) and sales to listings ratio of 42% compared to 19% in January 2026, 36% in February 2025, 46% in February 2024 and 52% in February 2023.

North Vancouver: Total Units Sold in February were 135, up from 92 (47%) in January, up from 125 (8%) in December, down from 158 (15%) in November, down from 153 (12%) in February 2025, down from 163 (17%) in February 2024, and down from 150 (10%) in February 2023; Active Listings were at 790 at month end compared to 684 at that time last year (up 15%) and 696 at the end of January (up 14%); the 402 New Listings in February were down 1% compared to January, up 253% compared to December, up 39% compared to November, up 14% compared to February 2025, up 17% compared to February 2024 and up 58% compared to February 2023. Month’s supply of total residential listings is down to 6 months from 8 (balanced market conditions) and sales to listings ratio of 34% compared to 23% in January 2026, 43% in February 2025, 48% in February 2024 and 59% in February 2023.

West Vancouver: Total Units Sold in February were 33, up from 29 (14%) in January, up from 28 (18%) in December, down from 53 (38%) in November, down from 39 (15%) in February 2025, down from 56 (41%) in February 2024, and down from 43 (23%) in February 2023; Active Listings were at 581 at month end compared to 580 at that time last year and 557 at the end of January (up 4%); the 159 New Listings in February were down 25% compared to January, up 148% compared to December, up 37% compared to November, down 10% compared to February 2025, down 7% compared to February 2024 and up 3% compared to February 2023. Month’s supply of total residential listings is down to 18 months from 19 (buyer’s market conditions) and sales to listings ratio of 21% compared to 14% in January 2026, 22% in February 2025, 33% in February 2024 and 28% in February 2023.

Richmond: Total Units Sold in February were 143, up from 129 (11%) in January, down from 165 (13%) in December, down from 191 (25%) in November, down from 179 (20%) in February 2025, down from 231 (38%) in February 2024, and down from 227 (37%) in February 2023; Active Listings were at 1,786 at month end compared to 1,513 at that time last year (up 18%) and 1,684 at the end of January (up 6%); the 515 New Listings in February were down 14% compared to January, up 94% compared to December, up 18% compared to November, down 14% compared to February 2025, up 11% compared to February 2024 and up 12% compared to February 2023. Month’s supply of total residential listings is down to 12 months from 13 (buyer’s market conditions) and sales to listings ratio of 28% compared to 22% in January 2026, 30% in February 2025, 50% in February 2024 and 49% in February 2023.

Burnaby East: Total Units Sold in February were 19, up from 9 (111%) in January, up from 15 (27%) in December, up from 18 (6%) in November, down from 21 (10%) in February 2025, down from 25 (24%) in February 2024, and down from 21 (15%) in February 2023; Active Listings were at 162 at month end compared to 153 at that time last year (up 6%) and 141 at the end of January (up 7%); the 69 New Listings in February were up 6% compared to January, up 165% compared to December, up 109% compared to November, up 6% compared to February 2025, up 15% compared to February 2024 and up 245% compared to February 2023. Month’s supply of total residential listings is down to 9 months from 16 (buyer’s market conditions) and sales to listings ratio of 28% compared to 14% in January 2026, 32% in February 2025, 42% in February 2024 and 105% in February 2023.

Burnaby North: Total Units Sold in February were 97, up from 80 (21%) in January, down from 113 (14%) in December, down from 98 (1%) in November, down from 129 (25%) in February 2025, down from 121 (20%) in February 2024, and down from 134 (28%) in February 2023; Active Listings were at 772 at month end compared to 728 at that time last year (up 6%) and 715 at the end of January (up 8%); the 284 New Listings in February were down 17% compared to January, up 127% compared to December, up 19% compared to November, down 12% compared to February 2025, up 14% compared to February 2024 and up 39% compared to February 2023. Month’s supply of total residential listings is down to 8 months from 9 (buyer’s market conditions) and sales to listings ratio of 34% compared to 23% in January 2026, 40% in February 2025, 49% in February 2024 and 66% in February 2023.

Burnaby South: Total Units Sold in February were 85, up from 67 (27%) in January, the same as December, down from 89 (4%) in November, up from 75 (13%) in February 2025, down from 109 (22%) in February 2024, and down from 118 (28%) in February 2023; Active Listings were at 643 at month end compared to 597 at that time last year (up 8%) and 604 at the end of January (up 6%); the 215 New Listings in February were down 16% compared to January, up 111% compared to December, up 31% compared to November, down 13% compared to February 2025, up 3% compared to February 2024 and up 4% compared to February 2023. Month’s supply of total residential listings is down to 8 months from 9 (buyer’s market conditions) and sales to listings ratio of 40% compared to 26% in January 2026, 30% in February 2025, 52% in February 2024 and 57% in February 2023.

New Westminster: Total Units Sold in February were 76, up from 48 (58%) in January, up from 67 (13%) in December, up from 65 (17%) in November, down from 88 (14%) in February 2025, down from 79 (4%) in February 2024, and up from 66 (15%) in February 2023; Active Listings were at 515 at month end compared to 448 at that time last year (up 15%) and 464 at the end of January (up 11%); the 227 New Listings in February were up 4% compared to January, up 203% compared to December, up 69% compared to November, down 10% compared to February 2025, up 19% compared to February 2024 and up 112% compared to February 2023. Month’s supply of total residential listings is down to 7 months from 10 (balanced market conditions) and sales to listings ratio of 33% compared to 22% in January 2026, 43% in February 2025, 41% in February 2024 and 62% in February 2023.

Coquitlam: Total Units Sold in February were 163, up from 89 (83%) in January, up from 149 (9%) in December, up from 146 (12%) in November, down from 165 (1%) in February 2025, down from 189 (14%) in February 2024, and up from 158 (3%) in February 2023; Active Listings were at 1,116 at month end compared to 1,049 at that time last year (up 6%) and 1,063 at the end of January (up 5%); the 418 New Listings in February were down 7% compared to January, up 143% compared to December, up 15% compared to November, down 11% compared to February 2025, up 13% compared to February 2024 and up 76% compared to February 2023. Month’s supply of total residential listings is down to 7 months from 12 (balanced market conditions) and sales to listings ratio of 39% compared to 20% in January 2026, 35% in February 2025, 51% in February 2024 and 67% in February 2023.

Port Moody: Total Units Sold in February were 36, up from 25 (44%) in January, down from 50 (28%) in December, down from 46 (28%) in November, down from 40 (10%) in February 2025, down from 46 (22%) in February 2024, and down from 47 (23%) in February 2023; Active Listings were at 308 at month end compared to 233 at that time last year (up 32%) and 291 at the end of January (up 6%); the 135 New Listings in February were down 7% compared to January, up 141% compared to December, up 24% compared to November, down 12% compared to February 2025, up 67% compared to February 2024 and up 48% compared to February 2023. Month’s supply of total residential listings is down to 9 months from 12 (buyer’s market conditions) and sales to listings ratio of 27% compared to 17% in January 2026, 33% in February 2025, 57% in February 2024 and 52% in February 2023.

Port Coquitlam: Total Units Sold in February were 46, up from 28 (64%) in January, up from 43 (7%) in December, down from 61 (25%) in November, down from 58 (21%) in February 2025, down from 64 (28%) in February 2024, and up from 40 (15%) in February 2023; Active Listings were at 309 at month end compared to 262 at that time last year (up 18%) and 304 at the end of January (up 2%); the 100 New Listings in February were down 40% compared to January, up 75% compared to December, up 9% compared to November, down 22% compared to February 2025, down 33% compared to February 2024 and up 15% compared to February 2023. Month’s supply of total residential listings is down to 7 months from 11 (balanced market conditions) and sales to listings ratio of 46% compared to 17% in January 2026, 45% in February 2025, 43% in February 2024 and 46% in February 2023.

Pitt Meadows: Total Units Sold in February were 13, up from 9 (44%) in January, down from 16 (19%) in December, down from 28 (54%) in November, down from 21 (38%) in February 2025, down from 23 (43%) in February 2024, and down from 15 (13%) in February 2023; Active Listings were at 128 at month end compared to 84 at that time last year (up 52%) and 96 at the end of January (up 33%); the 69 New Listings in February were up 30% compared to January, up 475% compared to December, up 97% compared to November, up 56% compared to February 2025, up 53% compared to February 2024 and up 156% compared to February 2023. Month’s supply of total residential listings is down to 10 months from 11 (buyer’s market conditions) and sales to listings ratio of 18% compared to 16% in January 2026, 47% in February 2025, 51% in February 2024 and 55% in February 2023.

Maple Ridge: Total Units Sold in February were 105, up from 72 (46%) in January, up from 78 (35%) in December, up from 100 (5%) in November, down from 129 (19%) in February 2025, down from 145 (28%) in February 2024, and down from 129 (19%) in February 2023; Active Listings were at 769 at month end compared to 735 at that time last year (up 4%) and 733 at the end of January (up 5%); the 279 New Listings in February were the same as January, up 179% compared to December, up 39% compared to November, down 10% compared to February 2025, down 30% compared to February 2024 and up 34% compared to February 2023. Month’s supply of total residential listings is down to 7 months from 10 (balanced market conditions) and sales to listings ratio of 37% compared to 25% in January 2026, 41% in February 2025, 36% in February 2024 and 62% in February 2023.

Ladner: Total Units Sold in February were 26, up from 5 (420%) in January, up from 7 (271%) in December, down from 27 (4%) in November, down from 29 (10%) in February 2025, up from 23 (13%) in February 2024, and down from 27 (4%) in February 2023; Active Listings were at 154 at month end compared to 146 at that time last year (up 5%) and 147 at the end of January (up 5%); the 60 New Listings in February were down 17% compared to January, up 400% compared to December, up 15% compared to November, down 9% compared to February 2025, up 62% compared to February 2024 and down 2% compared to February 2023. Month’s supply of total residential listings is down to 6 months from 29 (balanced market conditions) and sales to listings ratio of 43% compared to 7% in January 2026, 44% in February 2025, 62% in February 2024 and 44% in February 2023.

Tsawwassen: Total Units Sold in February were 27, up from 19 (42%) in January, down from 29 (7%) in December, down from 30 (10%) in November, down from 28 (4%) in February 2025, down from 38 (29%) in February 2024, and up from 25 (8%) in February 2023; Active Listings were at 275 at month end compared to 245 at that time last year (up 12%) and 255 at the end of January (up 8%); the 98 New Listings in February were up 11% compared to January, up 326% compared to December, up 48% compared to November, the same as February 2025, up 31% compared to February 2024 and up 85% compared to February 2023. Month’s supply of total residential listings is down to 10 months from 13 (buyer’s market conditions) and sales to listings ratio of 28% compared to 22% in January 2026, 29% in February 2025, 51% in February 2024 and 47% in February 2023.

Fraser Valley: Sales in February were up 36% at 843 compared to January at 619 and were down 8% from February 2025 at 920. New listings were down 9% at 2,796 from January at 3,078 and down 10% from February 2025 at 3,121. The average price of $913,110 was down 3% month-over-month and was down 8% year-over-year. Active listings at 8,344 were up 8% compared to last month at 7,711 and up 3% from February 2025 at 8,070. Month’s supply of total residential listings is down to 10 months supply from 12 in January (buyer’s market conditions).