Highlights of Dexter’s March 2025 report

Sales in March up 14% month-over-month

Best market for buyers in years

New listings continue to be on the rise

Time to move on from tariffs

When Phil Collins came out with the hit song Land of Confusion in 1986 (highly recommend watching the video), who knew it was 39 years early! With politics on both sides of the border creating distraction and confusion for buyers and sellers, a solution might be to listen to more music and less news! Although as of April 2nd, the confusion may have come to an end as the U.S. tariff announcement came, and Canada seems to be in a better position than anticipated with the CUSMA free trade agreement mostly upheld and other tariffs levied around escaping Canadian imports. Yes, we still have tariffs in place but it may just be time to get this market started!

Moving to politics in our country, we can expect a whole host of promises to come this month as the Conservatives and Liberals try to sway voters their way. Housing will be a hot topic for both parties as they try to convince Canadians they have a better model for easing affordability and supply issues in Canadian markets. GST cuts have been promised on new homes, capital gains relief and boosting supply through higher construction targets. Expect some of this might stick when a new government is formed. Whichever party forms government, hopefully they realize that investment in Canada is going to be a key piece moving forward. If we want capital to come to Canada, we need to incentivize it, and the housing market is one avenue that needs to be considered.

There were 2,091 properties sold in Greater Vancouver in March, after 1,827 properties sold in February, 1,552 properties sold in January, 1,765 properties sold in December, and 2,181 properties sold in November. Spring break and tariff talk held back buyer activity in March, and while spring break typically keeps buyers preoccupied, it was mostly the uncertainty of tariffs that continued to affect buyers. Perhaps the noise will quiet down enough to bring more buyers back. They are certainly out there and just needing a reason to jump back into the market. The Bank of Canada is doing their part. The campaign promises in Canada could also help kick start buyers.

Greater Vancouver home sales while up over the last 3 months, were below the total sales for the last two years in March. This was not unexpected though and while lower, there is still an opportunity to see an improvement in April. Sales in March were down 13% compared to March 2024 with 2,415 homes sold and down from March 2023 which saw 2,535 sales. This is the second straight month that sales lagged the previous year after January was 9% higher compared to the 1,427 properties sold in January 2024 and a 51% increase from the 1,030 sales in January 2023. Without tariff talk, this would be a completely different real estate market and it could be going forward – but in a positive direction. Buyers enjoy the moment, because it won’t last. Heading east, the Fraser Valley region saw sales in March down 26% compared to March 2024 after being down 27% year-over-year in February.

Greater Vancouver sales in March were 35% below the 10-year average compared to February at 39% below the 10-year average and January where sales were 29% below the 10-year average. This was the second lowest total sales for the month of March going back to 1986, with March 2019 being the lowest at 1,743 sales that year. Given how much more is happening this March with the political uncertainty, it’s encouraging that sales for this March were higher than 2019.

Greater Vancouver sellers were much more active in March compared to buyers. There were 6,565 new listings in March compared with 5,163 new listings in February. And with sales levels still lagging this past month, the absorption rate of new listings dropped in March with 32% of new listings being purchased, compared to 35% in February and 47% in March 2024. That percentage favours buyers that are serious in this market as it allows the inventory of homes available to grow and thus provide much more opportunity for buyers to negotiate on the home they want. Other than the super heated market of 2021 and 2022, the number of new listings for the month of March haven’t been that high since 2010 and 2011. New listings in March this year were significantly higher compared to the 5,112 and 4,427 in March 2024 and 2023 respectively.

The number of new listings in March were 15% above the 10-year average, compared with February which were 12% above the 10-year average, and January which saw the number of new listings 30% above the 10-year average. With total listings well below the all-time highs, it is keeping the real estate market in a balanced to border line buyer’s market. Owning real estate is still a sound investment. And don’t listen to the news story that mortgage delinquencies are on the rise. In British Columbia, mortgages in arrears are only 0.19% of all mortgages. That’s 7 times lower than the United States. So that’s not driving listings counts. And with B.C. lower than the national rate of delinquency, we won’t be seeing any real uptick in distressed home sales.

There were 14,546 active listings in Greater Vancouver at month end, compared to 12,744 at the end of February. Total active listings are up from 10,552 at the end of March last year, a 38% increase year-over-year. This year-over-year increase was almost as high as what we saw between March 2018 and 2019 – the highest going back to over 30 years. Finally, buyers have choice and opportunity. With lower interest rates and less competition for now, this is the best buying opportunity we’ve seen in some time.

Months of supply remained at 7 months in Greater Vancouver due to the uptick in sales and despite higher inventory numbers. The detached market in Greater Vancouver bumped up to 10 from 9 months supply, while townhomes stayed at 5 months and condos also held, staying at 6 months. Townhomes will continue to be undersupplied in the market, especially in Greater Vancouver as land prices make it more challenging to develop. In the Fraser Valley, months of supply is at 9, while detached is at 10 months supply, townhomes are at 5 months and condos are at 7 months.

With the push for more purpose-built rental buildings over the last few years, there are fewer new strata ownership units being built which will keep supply constrained in the coming years. Even with the increase in listings and slower activity, what’s most affordable is still the hardest to get into. This could be the opportunity for the presale market to jump back into the picture, with the help of higher GST exemptions for buyers and the promise of lower development costs charges by the Federal Liberals.

Greater Vancouver townhome sales in March were down 4% compared to March last year, while condos sales were down 10% year-over-year. Detached sales struggled the most in March, down 24% from March last year. Townhome inventory overall was up 39% year-over year compared to 34% at the end of February, while condo inventory climbed to 42% above March 2024 after being up 37% in February year-over-year. Detached homes were up 33% year-year-year, compared to 27% at the end of February above the previous year. Over in the Fraser Valley, detached home inventory is up 51% year-over-year while townhome inventory is up 72% and condo inventory is up 67%. Buyers have even greater opportunities in the Fraser Valley. Expect to see sales increase in the coming months.

The Greater Vancouver real estate market is showing resilience despite recent political and economic uncertainties. With the U.S. tariff announcement bringing clarity and the CUSMA trade agreement mostly upheld, confidence could begin to return. While sales in March remained below last year’s levels, they have been gradually increasing over the past three months, and an influx of new listings is giving buyers more choices and negotiating power. Political parties in Canada are focusing on housing policies, which could further support the market. With stable mortgage delinquency rates, balanced conditions, and potential interest rate declines, this may be one of the best opportunities for buyers in recent years.

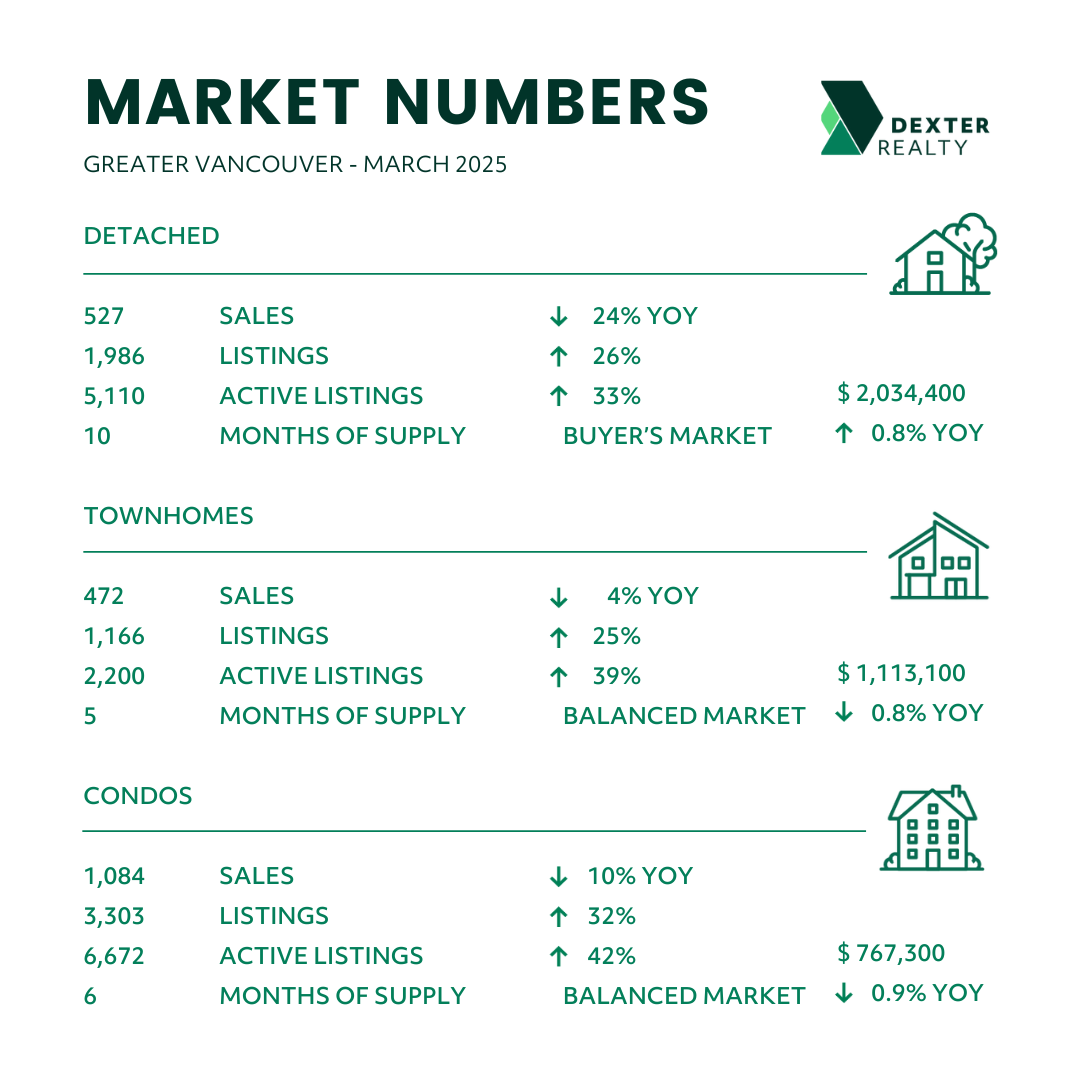

Here’s a summary of the numbers:

Greater Vancouver: Total Units Sold in March were 2,091 – up from 1,827 (14%) in February, up from 1,552 (35%) in January, down from 2,415 (13%) in March 2024, and down from 2,535 (18%) in March 2023; Active Listings were at 14,546 at month end compared to 10,552 at that time last year (up 38%) and 12,744 at the end of February (up 14%); the 6,565 New Listings in March were up 27% compared to February 2025, up 28% compared to March 2024, and up 48% compared to March 2023. Month’s supply of total residential listings is steady at 7 month’s supply (balanced market conditions) and sales to listings ratio of 32% compared to 35% in February, 47% in March 2024, and 57% in March 2023.

Month-over-month, the house price index is up 0.5% and in the last 6 months up 1.0%.

Vancouver Westside: Total Units Sold in March were 394 – up from 307 (28%) in February, up from 255 (55%) in January, down from 424 (7%) in March 2024, and down from 449 (12%) in March 2023; Active Listings were at 3,098 at month end compared to 2,342 at that time last year (up 32%) and 2,780 at the end of February (up 11%); the 1,315 New Listings in March were up 23% compared to February 2025, up 35% compared to March 2024, and up 42% compared to March 2023. Month’s supply of total residential listings is down to 8 month’s supply from 9 (buyer’s market conditions) and sales to listings ratio of 30% compared to 29% in February, 44% in March 2024, and 49% in March 2023.

Month-over-month, the house price index is up 0.5% and in the last 6 months up 2.0%.

Vancouver East Side: Total Units Sold in March were 247 – up from 204 (21%) in February, up from 158 (56%) in January, down from 285 (13%) in March 2024, and down from 287 (14%) in March 2023; Active Listings were at 1,494 at month end compared to 1,198 at that time last year (up 25%) and 1,313 at the end of February (up 14%); the 733 New Listings in March were up 29% compared to February 2025, up 23% compared to March 2024, and up 59% compared to March 2023. Month’s supply of total residential listings is steady at 6 month’s supply (balanced market conditions) and sales to listings ratio of 33% compared to 36% in February, 48% in March 2024, and 62% in March 2023.

Month-over-month, the house price index is up 0.4% and in the last 6 months up 1.3%.

North Vancouver: Total Units Sold in March were 171 – up from 153 (12%) in February, up from 148 (16%) in January, down from 187 (9%) in March 2024, and down from 215 (20%) in March 2023; Active Listings were at 844 at month end compared to 523 at that time last year (up 61%) and 684 at the end of February (up 23%); the 512 New Listings in March were up 45% compared to February 2025, up 54% compared to March 2024, and up 39% compared to March 2023. Month’s supply of total residential listings is up to 5 month’s supply from 4 (balanced market conditions) and sales to listings ratio of 33% compared to 43% in February, 56% in March 2024, and 58% in March 2023.

Month-over-month, the house price index is up 0.5% and in the last 6 months up 2.8%.

West Vancouver: Total Units Sold in March were 40 – up from 39 (3%) in February, up from 30 (33%) in January, down from 53 (25%) in March 2024, and down from 64 (37%) in March 2023; Active Listings were at 626 at month end compared to 560 at that time last year (up 12%) and 580 at the end of February (up 8%); the 206 New Listings in March were up 16% compared to February 2025, up 10% compared to March 2024, and up 26% compared to March 2023. Month’s supply of total residential listings is up to 16 month’s supply from 15 (buyer’s market conditions) and sales to listings ratio of 19% compared to 22% in February, 28% in March 2024, and 39% in March 2023.

Month-over-month, the house price index is up 0.2% but in the last 6 months down 0.4%.

Richmond: Total Units Sold in March were 220 – up from 179 (23%) in February, up from 206 (7%) in January, down from 279 (21%) in March 2024, and down from 352 (37%) in March 2023; Active Listings were at 1,728 at month end compared to 1,166 at that time last year (up 48%) and 1,513 at the end of February (up 14%); the 733 New Listings in March were up 22% compared to February 2025, up 32% compared to March 2024, and up 53% compared to March 2023. Month’s supply of total residential listings is steady at 8 month’s supply (buyer’s market conditions) and sales to listings ratio of 30% compared to 30% in February, 50% in March 2024, and 74% in March 2023.

Month-over-month, the house price index is up 0.8% and in the last 6 months down 0.3%.

Burnaby East: Total Units Sold in March were 27 – up from 21 (29%) in February, up from 17 (59%) in January, down from 32 (16%) in March 2024, and up from 20 (35%) in March 2023; Active Listings were at 174 at month end compared to 101 at that time last year (up 72%) and 153 at the end of February (up 14%); the 85 New Listings in March were up 31% compared to February 2025, up 60% compared to March 2024, and up 81% compared to March 2023. Month’s supply of total residential listings is down to 6 month’s supply from 7 (balanced market conditions) and sales to listings ratio of 31% compared to 32% in February, 60% in March 2024, and 43% in March 2023.

Month-over-month, the house price index is up 0.2% and in the last 6 months down 0.2%.

Burnaby North: Total Units Sold in March were 107 – down from 129 (17%) in February, up from 104 (3%) in January, down from 109 (2%) in March 2024, and down from 169 (37%) in March 2023; Active Listings were at 878 at month end compared to 535 at that time last year (up 64%) and 728 at the end of February (up 21%); the 427 New Listings in March were up 33% compared to February 2025, up 40% compared to March 2024, and up 79% compared to March 2023. Month’s supply of total residential listings is up to 8 month’s supply from 6 (buyer’s market conditions) and sales to listings ratio of 25% compared to 40% in February, 36% in March 2024, and 71% in March 2023.

Month-over-month, the house price index is up 0.7% and in the last 6 months up 1.2%.

Burnaby South: Total Units Sold in March were 94 – up from 75 (25%) in February, up from 59 (59%) in January, down from 142 (29%) in March 2024, and down from 130 (28%) in March 2023; Active Listings were at 671 at month end compared to 446 at that time last year (up 50%) and 597 at the end of February (up 12%); the 285 New Listings in March were up 15% compared to February 2025, up 16% compared to March 2024, and up 20% compared to March 2023. Month’s supply of total residential listings is down to 7 month’s supply from 8 (balanced market conditions) and sales to listings ratio of 32% compared to 30% in February, 58% in March 2024, and 55% in March 2023.

Month-over-month, the house price index is down 0.1% and in the last 6 months up 2.1%.

New Westminster: Total Units Sold in March were 104 – up from 88 (18%) in February, up from 61 (70%) in January, down from 108 (4%) in March 2024, and up from 96 (8%) in March 2023; Active Listings were at 513 at month end compared to 350 at that time last year (up 47%) and 448 at the end of February (up 15%); the 269 New Listings in March were up 30% compared to February 2025, up 27% compared to March 2024, and up 91% compared to March 2023. Month’s supply of total residential listings is steady at 5 month’s supply (balanced market conditions) and sales to listings ratio of 38% compared to 43% in February, 51% in March 2024, and 68% in March 2023.

Month-over-month, the house price index is down 0.1% and in the last 6 months down 2.2%.

Coquitlam: Total Units Sold in March were 233 – up from 165 (41%) in February, up from 155 (50%) in January, down from 235 (1%) in March 2024, and up from 196 (19%) in March 2023; Active Listings were at 1,173 at month end compared to 663 at that time last year (up 77%) and 1,049 at the end of February (up 12%); the 593 New Listings in March were up 26% compared to February 2025, up 40% compared to March 2024, and up 94% compared to March 2023. Month’s supply of total residential listings is down to 5 month’s supply from 6 (balanced market conditions) and sales to listings ratio of 39% compared to 35% in February, 55% in March 2024, and 64% in March 2023.

Month-over-month, the house price index is down 0.1% and in the last 6 months down 0.1%.

Port Moody: Total Units Sold in March were 51 – up from 40 (28%) in February, up from 32 (59%) in January, up from 45 (13%) in March 2024, and down from 80 (36%) in March 2023; Active Listings were at 279 at month end compared to 160 at that time last year (up 74%) and 233 at the end of February (up 20%); the 152 New Listings in March were up 26% compared to February 2025, up 45% compared to March 2024, and up 33% compared to March 2023. Month’s supply of total residential listings is down to 5 month’s supply from 6 (balanced market conditions) and sales to listings ratio of 33% compared to 33% in February, 43% in March 2024, and 70% in March 2023.

Month-over-month, the house price index is up 0.4% and in the last 6 months down 4.4%.

Port Coquitlam: Total Units Sold in March were 62 – up from 58 (7%) in February, down from 65 (5%) in January, down from 89 (30%) in March 2024, and down from 69 (10%) in March 2023; Active Listings were at 313 at month end compared to 213 at that time last year (up 47%) and 262 at the end of February (up 19%); the 176 New Listings in March were up 36% compared to February 2025, up 26% compared to March 2024, and up 39% compared to March 2023. Month’s supply of total residential listings is steady at 5 month’s supply (balanced market conditions) and sales to listings ratio of 35% compared to 45% in February, 64% in March 2024, and 54% in March 2023.

Month-over-month, the house price index is down 0.1% and in the last 6 months up 1.6%.

Pitt Meadows: Total Units Sold in March were 27 – up from 21 (29%) in February, up from 13 (108%) in January, down from 29 (7%) in March 2024, and down from 28 (4%) in March 2023; Active Listings were at 105 at month end compared to 66 at that time last year (up 59%) and 84 at the end of February (up 25%); the 66 New Listings in March were up 50% compared to February 2025, up 57% compared to March 2024, and up 53% compared to March 2023. Month’s supply of total residential listings is steady at 4 month’s supply (seller’s market conditions) and sales to listings ratio of 40% compared to 47% in February, 69% in March 2024, and 65% in March 2023.

Month-over-month, the house price index is up 2.2% and in the last 6 months up 3.0%.

Maple Ridge: Total Units Sold in March were 108 – down from 129 (16%) in February, up from 95 (14%) in January, down from 187 (42%) in March 2024, and down from 149 (28%) in March 2023; Active Listings were at 832 at month end compared to 714 at that time last year (up 16%) and 735 at the end of February (up 13%); the 354 New Listings in March were up 13% compared to February 2025, down 4% compared to March 2024, and up 29% compared to March 2023. Month’s supply of total residential listings is up to 8 month’s supply from 6 (buyer’s market conditions) and sales to listings ratio of 30% compared to 41% in February, 50% in March 2024, and 60% in March 2023.

Month-over-month, the house price index is up 0.2% and in the last 6 months flat.

Ladner: Total Units Sold in March were 31 – up from 29 (7%) in February, up from 17 (82%) in January, up from 30 (3%) in March 2024, and down from 38 (19%) in March 2023; Active Listings were at 158 at month end compared to 90 at that time last year (up 76%) and 146 at the end of February (up 8%); the 68 New Listings in March were up 3% compared to February 2025, up 28% compared to March 2024, and down 1% compared to March 2023. Month’s supply of total residential listings is steady at 5 month’s supply (balanced market conditions) and sales to listings ratio of 45% compared to 44% in February, 57% in March 2024, and 55% in March 2023.

Month-over-month, the house price index is up flat and in the last 6 months down 1.3%.

Tsawwassen: Total Units Sold in March were 36 – up from 28 (29%) in February, up from 26 (38%) in January, up from 34 (6%) in March 2024, and up from 35 (3%) in March 2023; Active Listings were at 270 at month end compared to 172 at that time last year (up 57%) and 245 at the end of February (up 10%); the 99 New Listings in March were up 1% compared to February 2025, up 39% compared to March 2024, and up 21% compared to March 2023. Month’s supply of total residential listings is down to 8 month’s supply from 9 (buyer’s market conditions) and sales to listings ratio of 36% compared to 29% in February, 48% in March 2024, and 43% in March 2023.

Month-over-month, the house price index is up 0.5% and in the last 6 months up 0.6%.

Fraser Valley: Sales in March were up 12.6%, compared to February and were down 25.7% from March 2024. New listings were up 21.8% from February and up 27.3% from March 2024.The average price was up 3.5% month-over-month and is down 2.1% year-over-year. Active listings were up 14.2% to 9,219 from 8,070 last month and up 48.8% from March 2024 which was at 6,197. Month’s supply of total residential listings increased to 9 from 8 months (buyer’s market conditions).

Month-over-month, the house price index is up 0.4% and in the last 6 months down 0.5%.